From payday super to the $20k asset write-off, 2026 is a year of change for SMEs. Learn how experienced business owners are bridging the knowledge gap to adapt and grow.

At a glance

- Research shows 30% of business owners are unaware of the new Payday Super rules. Reviewing cash flow and updating payroll systems early can help avoid strict ATO penalties.

- Only 18% of SMEs plan to use the $20,000 instant asset write-off before 30 June. Making the most of it often involves sequencing equipment purchases against the upcoming cash flow changes.

- To manage the upcoming adjustments, many owners are reviewing their cash reserves and turning to flexible external funding to smooth out their cash flow this year.

2026 is a year of major shifts, with Payday Super and the upcoming instant asset write-off deadline creating both pressures and opportunities for Australian small businesses. According to the latest YouGov research commissioned by Prospa, 70% of business owners feel confident about maintaining positive cash flow over the next 12 months. However, 30% of business owners are unaware of the upcoming super changes, and nearly one in five admit their business is unprepared to pay superannuation on the same day as salary or wages are paid.

Here is a breakdown of what these changes mean, how other Australian SMEs are preparing, and the steps you can take to turn these challenges into an advantage.

What payday super means for your cash flow

For years, the three-month super payment cycle gave businesses a natural cash buffer. You could hold onto capital, manage day-to-day expenses, and smooth out your cash flow. From 1 July 2026, that flexibility disappears. Under the new Payday Super rules, employers must pay super contributions at the same time as salary and wages, ensuring funds reach employee accounts within seven business days.

Imagine a local cafe managing seasonal foot traffic. Under the quarterly system, a busy holiday period could easily subsidise the super liabilities built up during a quiet month. Come July, that cafe must fund its super obligations immediately, regardless of weekly sales dips or delayed supplier payments.

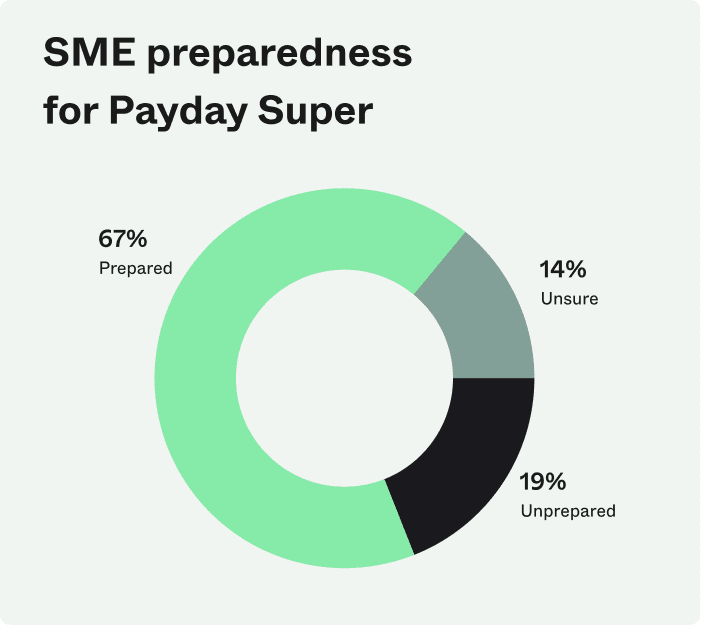

Missing the seven-day clearance window triggers immediate non-compliance, which can lead to strict penalties and additional charges. This explains why 19% of small businesses report they are not prepared for the shift, and a further 14% are unsure if they can meet the new payment schedule.

Source: YouGov SME Sentiment Research (Feb 2026)

How to get ahead:

Start by ensuring your payroll system can handle more frequent Single Touch Payroll reporting, and migrate away from the ATO’s clearing house before it closes on 30 June 2026. You will also need to review your cash flow to confirm you have enough liquidity to cover wages and the 12% super guarantee every pay cycle. Finally, educate your team and check your employee records to catch any inaccurate fund details now, preventing rejections that lead to costly non-compliance.

How the asset write-off deadline affects your EOFY plans

As the end of the financial year approaches, the $20,000 instant asset write-off offers a valuable opportunity to reduce your taxable income. It allows you to claim an immediate deduction for the business portion of eligible assets purchased before 30 June 2026.

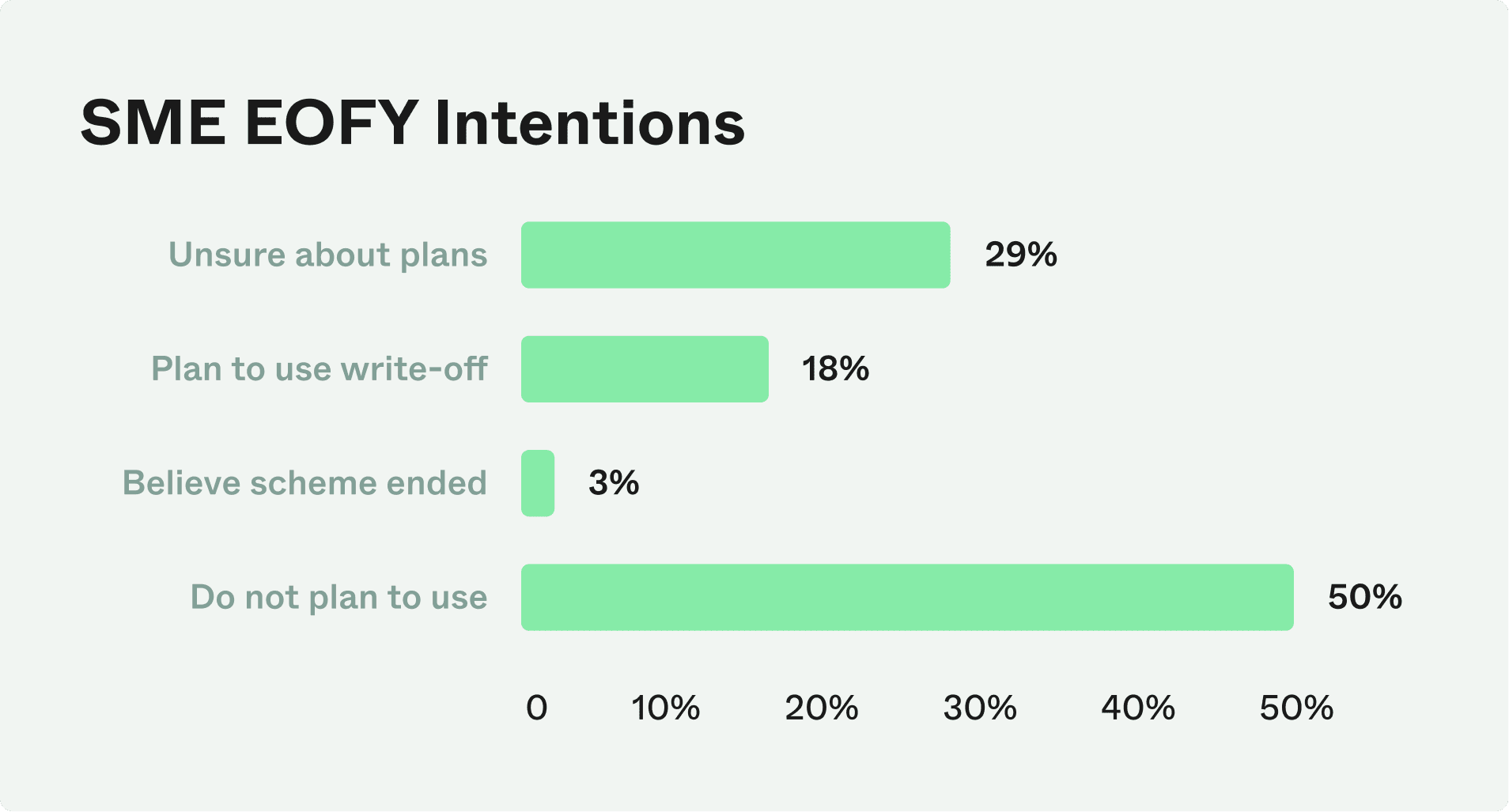

Despite the tax benefits, businesses are hesitating. Only 18% of SMEs plan to purchase eligible assets before the deadline. A further 29% are unsure about their plans, and 3% mistakenly believe the scheme has already ended. Intentions vary by sector. While 25% of professional services businesses plan to use the write-off, only 10% of those in retail and hospitality intend to do the same.

Source: YouGov SME Sentiment Research (Feb 2026)

With Payday Super accelerating cash outflows on 1 July, owners are stuck deciding whether to spend capital on equipment now or hold onto their working capital. For example, a tradie upgrading a work vehicle before June 30 secures the tax deduction. However, parting with that cash leaves them with less liquidity to cover their new, more frequent super obligations the following week.

How to get ahead:

Review your upcoming equipment needs against your current cash reserves. Map out your cash flow to see if the immediate tax benefit of an asset purchase outweighs the need for liquidity in July. If the numbers align, sequence your investments carefully to optimise your tax position before the new financial year begins.

Why your cash reserves need a review right now

On average, Australian business owners hold approximately 2.7 months’ worth of expenses in reserve. However, one in seven say their business has no cash reserves at all. A further 16% only have enough to cover less than a month of operational costs.

Aligning super obligations with pay cycles will impact your cash flow every week or fortnight. Businesses with thin buffers may find themselves squeezed. For a boutique retailer facing a slow sales month, covering payroll and superannuation payments at the same time can be very stressful.

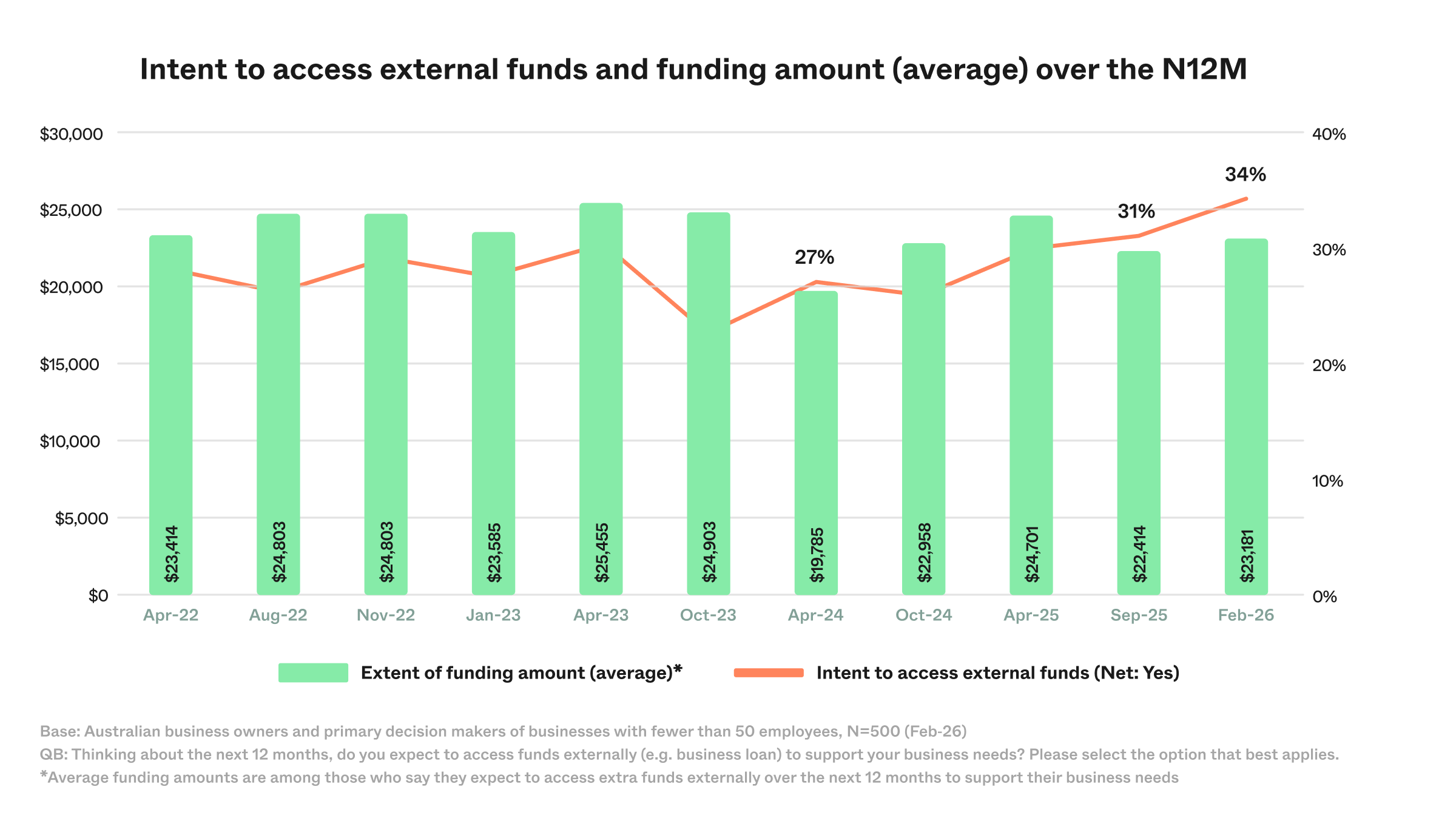

To bridge the gap between paying their team and receiving customer payments, many owners are looking for outside support. Intent to access external funding has trended upwards, with one in three SMEs expecting to secure finance over the next 12 months. Those planning to borrow expect to access an average of $23,181.

Source: YouGov SME Sentiment Research (Feb 2026)

How to get ahead:

Audit your current operating costs and aim to build a reserve that covers at least three to five months of expenses. If your cash flow is inconsistent, an option is to secure flexible funding before a shortfall happens. A business line of credit provides a safety net, allowing you to draw down funds to clear super contributions or urgent supplier invoices instantly without paying interest on the money you do not use.

Ready to build a stronger buffer for 2026?

A solid cash reserve means you don’t have to choose between making a much needed EOFY purchase and covering your new super obligations.

If your cash flow is looking tight, talk to the Prospa team to set up a flexible line of credit that keeps your business moving.