Should you buy or lease business equipment? Compare the pros, cons, and cash flow impact of each option to find the right fit for your business.

At a glance

- Buying business equipment costs less over time and builds asset value, but the upfront spend can strain your working capital when you need it most.

- Leasing keeps monthly costs predictable and lets you upgrade as technology changes, though you'll pay more overall and won't own the asset at the end.

- Many small businesses use a blended approach, buying long-life items and leasing fast-evolving tech, with financing options to bridge any cash flow gaps.

The right equipment helps your business run faster, serve more customers, and take on work you’d otherwise turn away. But paying for it upfront can tie up the cash you need for wages, rent, and day-to-day costs. And locking into a lease means paying more over time for something you’ll never own.

This guide breaks down the pros and cons of buying vs leasing, the questions worth asking before you commit, and how to finance a purchase if buying makes more sense but paying upfront doesn’t.

The case for buying business equipment

Buying equipment outright is straightforward: you pay for it, you own it. No ongoing lease payments, no end-of-term negotiations, no restrictions on how you use it. Over the life of the asset, buying is generally the cheaper option because you’re not paying a premium for the flexibility that leasing provides.

Take Priya, who runs a growing physiotherapy clinic in Brisbane. She’s expanding into a second treatment room and needs new treatment tables. These are sturdy, long-life items that won’t become outdated. Buying them can make more financial sense in this case: she pays once and gets a decade or more of use without another dollar going towards the equipment.

Ownership also means flexibility. Priya can modify the tables, move them between rooms, or sell them later if she upgrades. None of that is guaranteed with a lease.

Tax benefits of buying

When you purchase business equipment, you may be able to claim tax deductions that reduce the effective cost. Depreciation lets you spread the deduction across the asset’s useful life, and the Australian Government’s $20,000 instant asset write-off (extended for the 2025-26 financial year) lets eligible small businesses with an aggregated turnover under $10 million deduct the full cost of individual assets under $20,000 in the year they’re first used or installed ready for use.

The threshold applies per asset, so multiple purchases can each qualify. For more detail on eligibility and how it works, see our guide to the instant asset write-off.

Worth noting: the $20,000 threshold is currently set to drop back to $1,000 from 1 July 2026, so timing matters if you’re weighing up a purchase this financial year. Tax treatment depends on your business structure and circumstances, so talk to your accountant before making a decision based on tax alone.

The trade-off

Buying makes sense on paper, but it comes with a real cash flow trade-off. If Priya spends $12,000 on treatment tables the same month she’s paying a bond on her new room and covering a quiet patch between client bookings, that upfront cost can squeeze the cash she needs for wages and rent. That’s where financing the purchase, rather than paying from savings, can help bridge the gap. A small business loan lets you spread the cost while still owning the equipment from day one.

Buying works best for: equipment with a long useful life, stable technology, and low risk of becoming obsolete. Think commercial kitchen appliances, treatment tables, salon chairs, heavy tools, and fit-out furniture.

The case for leasing

Leasing lets you use the equipment you need without the upfront spend. Instead of a lump sum payment, you make regular, predictable instalments over a fixed term. At the end of the lease, you return the equipment, upgrade to something newer, or in some cases, buy it at an agreed residual price.

For Priya, not everything in her clinic has a ten-year lifespan. Her reception computer, practice management software setup, and portable EFTPOS terminal will all need replacing within three to four years as technology moves on. Leasing this equipment means she avoids paying full price for items she’ll outgrow, and the fixed monthly cost makes budgeting simpler.

Where leasing makes sense

Leasing can be the smarter choice when the asset depreciates quickly, when you need to stay current with evolving technology, or when preserving working capital is more important than long-term ownership. Some leases also include maintenance, which removes the risk of unexpected repair bills eating into your budget.

For businesses in a growth phase, leasing frees up cash that can go towards hiring, marketing, or stocking inventory, areas where the return on investment may be higher than locking funds into depreciating hardware.

The trade-offs

Over the full lease term, you’ll often pay more than the asset’s purchase price. You don’t build equity in the equipment, and ending a lease early can trigger penalties. There may also be restrictions on how you use or modify the asset during the term.

Different lease structures (operating leases, finance leases, hire purchase) come with different levels of ownership, flexibility, and tax treatment. For a detailed breakdown of how each type works, see our guide to asset finance.

Leasing works best for: fast-evolving technology (computers, POS systems, diagnostic equipment), short-term or project-based needs, and periods where cash flow is tight or unpredictable. Business equipment leasing in Australia is available through banks, specialist financiers, and equipment vendors, so it’s worth comparing terms before signing on.

Buying vs leasing: a side-by-side comparison

| Factor | Buying | Leasing |

|---|---|---|

| Upfront cost | Higher (full purchase price or deposit + finance) | Lower (little to no upfront cost) |

| Ongoing payments | None once paid off (or fixed loan repayments) | Regular lease payments for the full term |

| Total cost over time | Usually lower | Usually higher |

| Ownership | You own it outright | The lessor retains ownership |

| Technology risk | You carry the obsolescence risk | Easier to upgrade at end of term |

| Tax treatment | Depreciation or instant asset write-off may apply | Lease payments may be deductible as a business expense |

| Cash flow impact | Larger initial hit | Smaller, predictable payments |

| Flexibility | Full control: sell, modify, or repurpose any time | Locked into the lease term, with potential exit costs |

| Best for | Long-life assets with stable technology | Fast-changing tech and short-term needs |

There’s no single right answer when it comes to leasing vs buying equipment for a small business. The best choice depends on the equipment itself, how long you’ll use it, and what your cash flow looks like right now.

In practice, many businesses take a blended approach. Priya, for example, buys her treatment tables (long life, no tech risk) and leases her computer and POS setup (will need replacing in a few years). That way she owns what holds its value and keeps flexibility where it matters.

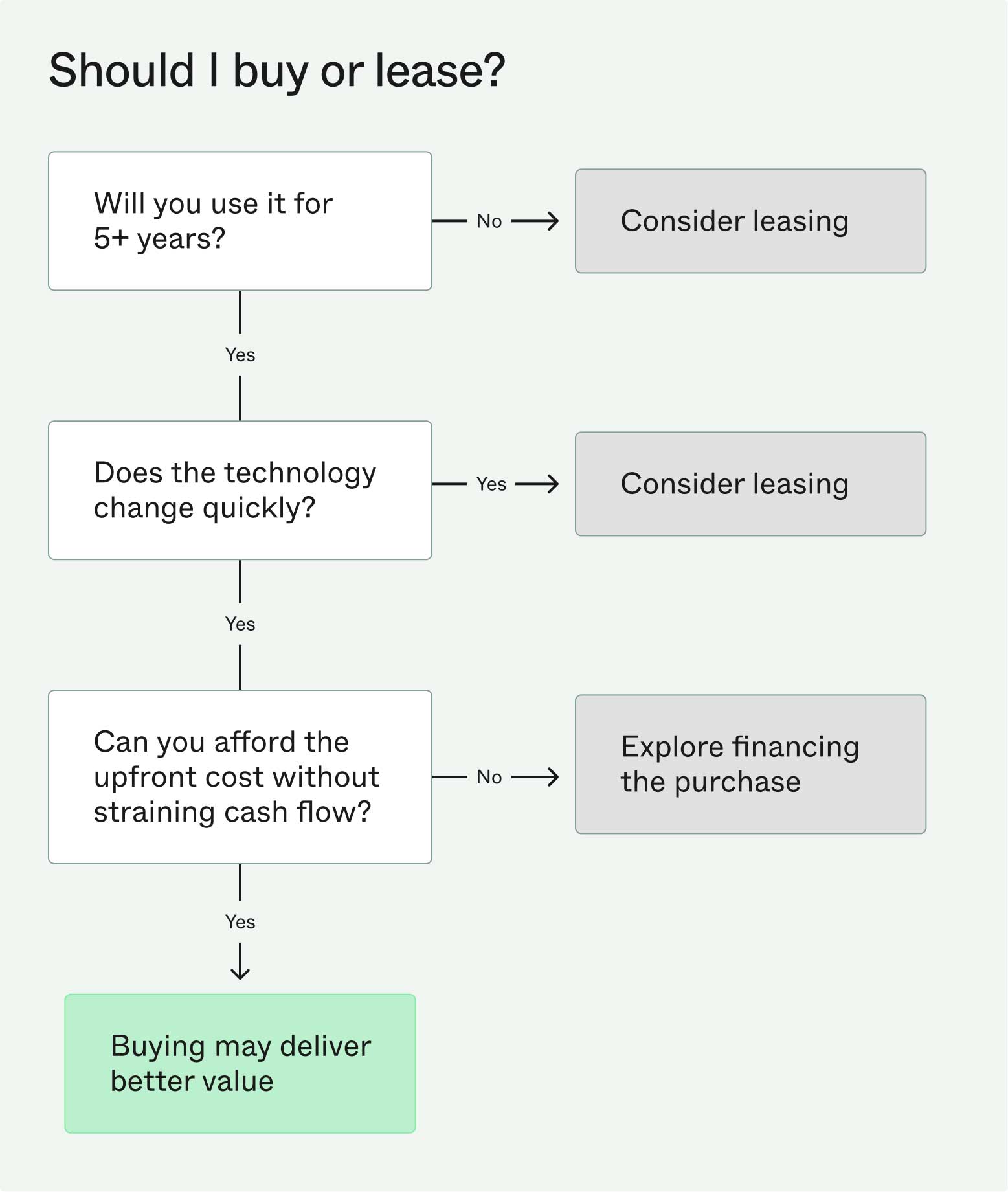

Five questions to ask before you decide

1. How long will you use the equipment?

Equipment you’ll use for five years or more may be worth owning, since there are no ongoing payments once it’s paid off. For shorter timeframes, leasing can avoid tying your money up in something you’ll need to replace soon anyway.

2. How quickly does it become obsolete?

A commercial-grade oven has a long shelf life. A laptop doesn’t. When technology moves fast, leasing gives you a built-in upgrade path at the end of each term, rather than being stuck with outdated hardware you’ve already paid full price for.

3. What’s your current cash flow position?

If a large upfront payment would leave you short on rent, wages, or supplier invoices, that’s a sign to consider either leasing or financing the purchase. A cash flow forecast can help you see the real impact before you commit. And if buying is the stronger long-term option but paying upfront isn’t realistic, a small business loan can let you own the asset while spreading the cost over time.

4. Do you want the asset on your balance sheet?

Owning equipment adds to your business assets, which can strengthen your position if you’re applying for finance or looking to sell the business down the track. Leasing (depending on the structure) may sit as an expense instead, so it’s worth understanding how each option flows through your financials before you commit.

5. What are the tax implications?

Buying may unlock depreciation deductions or the instant asset write-off for eligible assets under $20,000. Lease payments may be deductible as a business expense. The right answer depends on your business structure, turnover, and timing, so speak with your accountant about which path works better for your situation.

How to fund an equipment purchase without draining your cash flow

Buying often delivers better long-term value, but absorbing the full cost upfront can be difficult when you’re also covering rent, payroll, suppliers, and the everyday costs of running a business. Equipment finance for small businesses doesn’t have to mean a complex asset loan. Financing the purchase through a general-purpose business loan lets you get the equipment now, own it outright, and spread the cost into manageable repayments.

Prospa Small Business Loan

A Prospa Small Business Loan can suit a planned, one-off equipment purchase. You receive the funds as a lump sum, make fixed weekly repayments, and the equipment is yours from the start. Loans range from $5,000 to $500,000, with terms up to 5 years and no upfront security required for up to $150,000 in funding.

For Priya, this means she can cover her $12,000 fit-out in one go, spreading the cost across fixed weekly repayments she can plan around rather than draining her savings in a single hit.

Prospa business line of credit

If your equipment needs are ongoing or harder to predict, a business line of credit offers more flexibility. You draw funds as you need them and only pay interest on what you use. Limits range from $2,000 to $500,000, with a 2-year renewable term.

Priya sets up a business line of credit for smaller, less predictable purchases, like replacing a laptop when it dies or adding a new EFTPOS terminal for the second treatment room. She draws what she needs, when she needs it, and keeps the rest of her limit available for the next time something comes up.

Run the numbers first

Before you apply for any finance, it helps to see what repayments would look like for your business. Prospa’s loan calculator gives you a quick estimate so you can plan with confidence. For a broader look at the funding options available to Australian small businesses, our guide to business loans and financing options compares the most common paths side by side.

Ready to fund your next equipment purchase? Check your eligibility with Prospa in minutes