Manage Payday Super without the cash flow crunch

From 1 July 2026, super must be paid at the same time as wages. For businesses with tight margins or inconsistent revenue, that can create a real cash flow gap. Here's how you could avoid it.

Most businesses aren't ready for Payday Super

From 1 July 2026, Australian employers must pay superannuation at the same time as wages, so the quarterly buffer that’s given businesses breathing room for years is going away.

According to Prospa-YouGov research, 70% of business owners are confident about maintaining positive cash flow over the next 12 months. Yet 30% of SMEs are unaware of the Payday Super transition entirely, and nearly one in five admit their business is unprepared to meet the new payment schedule.

For businesses with thin margins, seasonal revenue, or clients who pay on 30-day terms, the loss of the quarterly buffer can create a real cash flow gap between when super is due and when money comes in. That’s where flexible funding can help.

Want to understand the full scope of the changes? Read our guide to Payday Super and what it means for your business.

Testimonial

"For businesses with thin buffers, moving super payments forward compresses working capital. The risk isn't the rule itself; it's being caught unprepared and being non-compliant."

Beau Bertoli

Co-Founder & Chief Revenue Officer

Already know what

you’re after? .

Need help?

Six ways businesses are using Prospa to stay covered

Payday Super creates new pressure points across your business. Here’s how Prospa’s funding solutions can help you manage them.

Bridge the gap when invoices are late

Avoid ATO penalties

Upgrade your payroll systems

Cover the transition period

Keep your team paid on time

Build a cash reserve before July

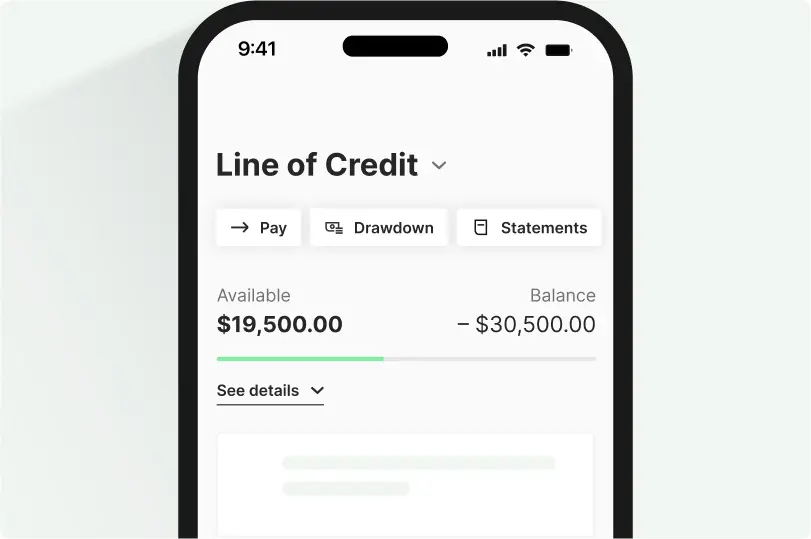

See how Prospa's Business Line of Credit compares

See how our features stack up and estimate what you’d pay per week.

| Prospa’s Line of Credit | Most other Lines of Credit | |

|---|---|---|

| Easy application | ||

| Funding in hours | ||

| Access up to your credit limit at anytime, for the entire term | ||

| Make payments directly from your Line of Credit | ||

| Lower your interest with unlimited extra repayments | ||

| Access funds 24/7 via the Prospa App | ||

| Integrates with Xero for easy accounting |

Your cash flow, your choice

Our calculator will help you estimate how much you’ll pay per week

See full T&CPlease select a product

Customers making it happen with a Prospa loan

Read customer stories

Awards, thanks to you

It’s nice to know we’re doing something right

| Year | Award | Category |

|---|---|---|

| 2024 | Great Place to Work | Certified |

| 2024 | The Adviser Magazine's Product of Choice: Non-Banks Survey | Winner, Best short-term loan |

| 2024 | The Adviser Magazine's Product of Choice: Non-Banks Survey | Winner, Best SME loans less than $250K |

| 2023 | LinkedIn Talent Awards | Winner, Best Employer Brand |

| 2020 | MFAA | Winner, MFAA State Excellence Awards |

July is closer than you think

The businesses that come through Payday Super in the best shape will be the ones that act now. Whether you need a funding safety net or want to talk through your options, we’re here to help.

FAQs

Common questions answered

From 1 July 2026, Australian employers must pay superannuation guarantee contributions at the same time as salary and wages, rather than quarterly. Contributions must reach employee super funds within seven business days of each payday.

Late payments can trigger the Superannuation Guarantee Charge (SGC), which includes the unpaid amount, daily compounding interest, and an administrative uplift of up to 60%. For company directors, unpaid SGC can also lead to personal liability through ATO Director Penalty Notices.

A business line of credit gives you ongoing access to funds you can draw on when you need them, and you only pay interest on what you use. This means if cash flow is tight on payday, you can cover super and wages without missing the deadline, then repay when client payments come through.

Yes. The Small Business Superannuation Clearing House (SBSCH) will no longer process payments after 30 June 2026, and it has already closed to new registrations. You’ll need to migrate to a commercial payroll or clearing house solution before the deadline.

Other questions?