A business loan costs more than just the interest rate. We break down application fees, ongoing charges, and other costs to give you a clear picture of what you'll really pay.

At a glance

- To determine the true cost of finance, make sure to look beyond the interest rate and account for establishment fees, ongoing charges, and conditional penalties.

- The total cost is also shaped by the loan type, whether it is secured or unsecured, the length of the repayment term, and its structure, either as a one-time loan or a revolving business line of credit.

- Your trading history, revenue, and credit score will also influence the rates and terms a lender can offer you.

In an era where AI can draft your emails and manage your schedule, you would expect comparing business loans to be just as straightforward. The reality, however, is that understanding the real cost of a loan isn’t as simple as pushing a button. Lenders present their products with different interest rates, fee structures, and repayment terms that can make a true side-by-side comparison difficult if you don’t know precisely what to look for.

This guide is designed to help you break down every component so you can assess the true cost of finance and confidently choose the right option for your business.

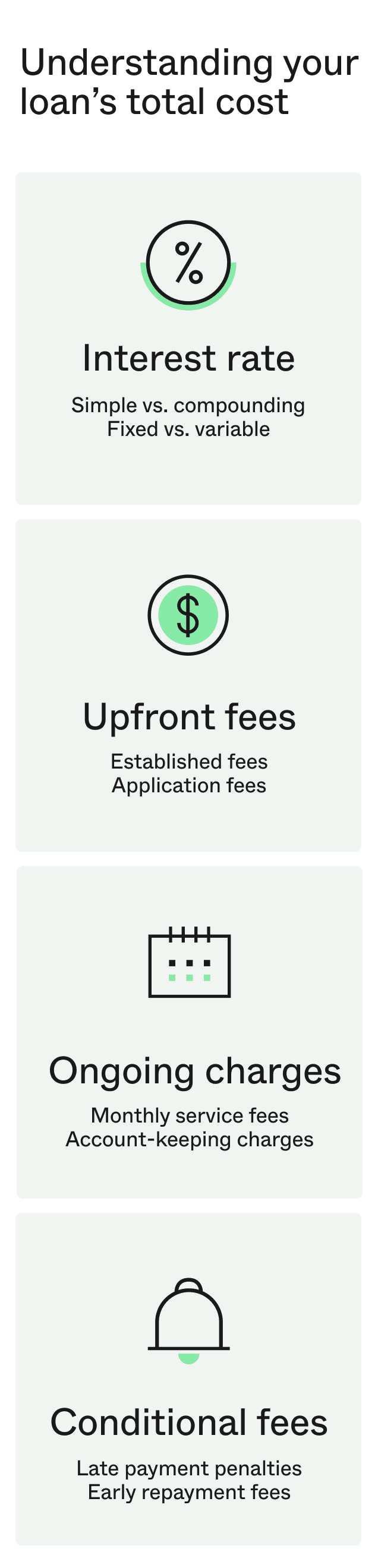

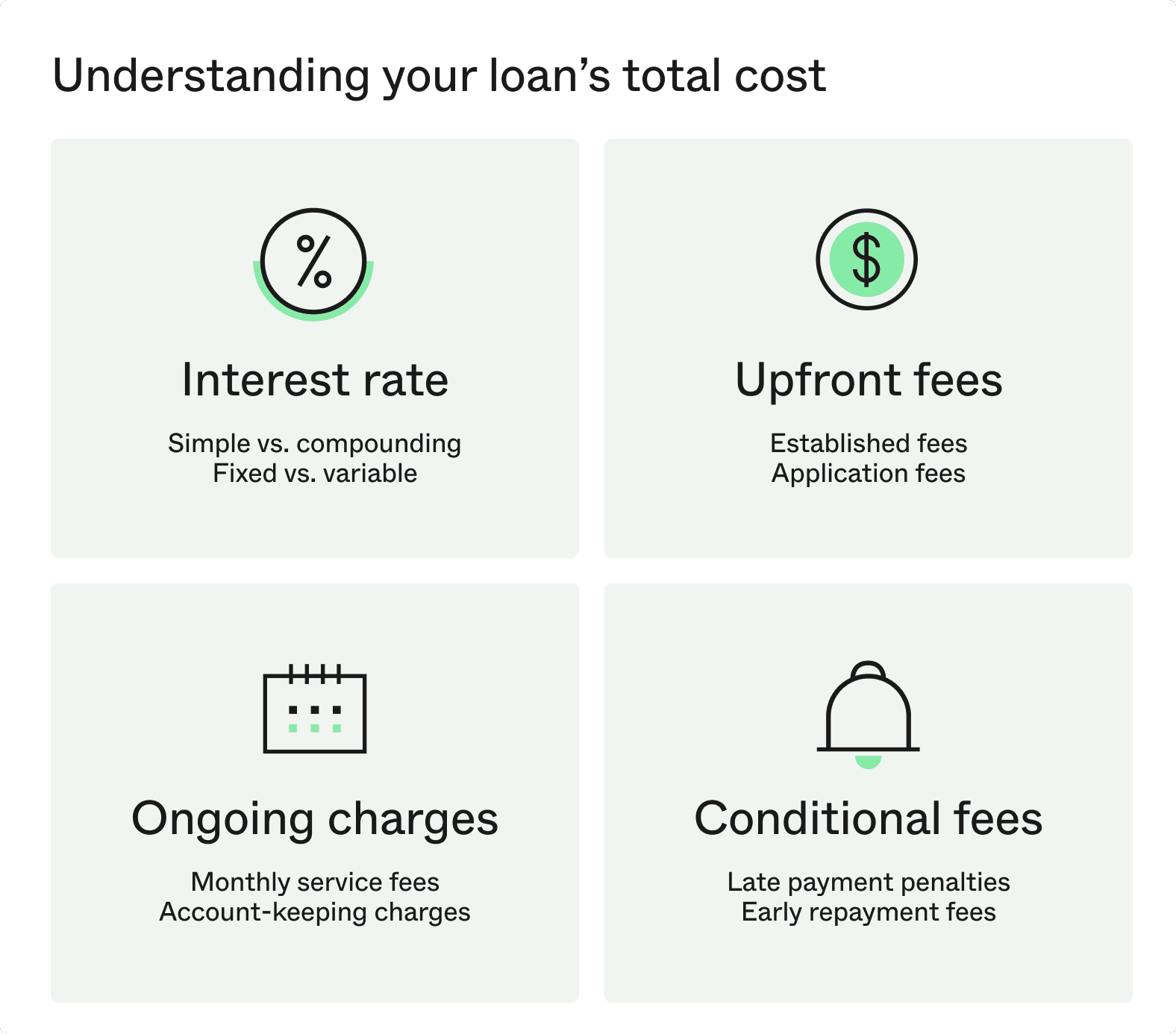

The key components of a business loan’s total cost

To accurately compare business loans, you need to understand the complete cost of borrowing, which means looking beyond the advertised interest rate to consider all associated fees and charges. Here is a breakdown of what to look for.

Interest rates explained

The interest rate is the percentage a lender charges for borrowing money, but how it’s calculated is what matters most. For example, on a $30,000 loan over one year at 15% p.a.:

- Simple interest is calculated on the original loan amount. The interest cost would be a straightforward $4,500.

- Compounding interest, calculated on the outstanding balance, would result in a higher total interest cost because you pay interest on the interest.

Many small business loans use simple interest for clarity. It’s also important to know if your rate is fixed (it’s agreed at the start and won’t change for the loan term) or variable (it can change based on market rates). Always ask the lender to confirm the total repayable amount for your exact term so you can compare like-for-like.

A note on terminology: Comparison rates are a consumer-credit concept. Business loans providers aren’t required to display a standardised comparison rate. If an Annual Percentage Rate (APR) is quoted, use it as an indicator, but base decisions on the total repayable, repayment schedule, and all fees and charges included in your loan.

Upfront fees

Many loans come with one-off fees charged at the start of the term. Often called an establishment, origination or application fee, this covers the lender’s cost of assessing and setting up the loan. For instance, a 3.5% origination fee on a $30,000 loan would be $1,050. This fee is sometimes added to the total loan balance.

Ongoing charges

Some products, particularly revolving credit facilities, may have regular fees. These can include monthly account-keeping fees or draw down fees charged each time you access funds. These ongoing charges contribute to the total cost and should be carefully reviewed. The Prospa Business Line of Credit, for example, has a small weekly fee (calculated as a percentage of your credit limit), which is important to factor into your total cost.

Potential penalty fees

You should also be aware of any conditional fees. Most lenders charge a fee for late or missed payments. Less obvious are early repayment fees. Some lenders apply a charge if you pay off a loan ahead of schedule, as this reduces the total interest they earn. Prospa does not charge a fee for making extra repayments on your Business Loan or Line of Credit and there are several other benefits of paying your business loan off early.

A practical example: How the costs add up

To see how these components come together, let’s consider a common scenario. Imagine you run a small cafe and need a $30,000 business loan to purchase a new commercial coffee machine and upgrade your point-of-sale system.

You secure a loan with a 12-month term. Here’s how the total cost could be broken down:

| Loan Component | Amount |

| Initial Loan Amount | $30,000 |

| Interest (15%) | $4,500 |

| Origination Fee (3.5%) | $1,050 |

| Total Repayable Amount | $35,550 |

| True cost of the loan | $5,550 |

In this scenario, the true cost of the loan is $5,550. Looking only at the interest would give you an incomplete picture of what you are agreeing to pay.

Wondering what your repayments could look like? Get an instant estimate with Prospa Business Loan Calculator

How different loan types affect what you’ll pay

The total cost of finance is heavily influenced by the type of product you choose. A loan designed for a large, long-term asset purchase will have a different cost structure from one designed to manage day-to-day cash flow.

Secured vs. unsecured loan costs

The presence of collateral — a business or personal asset used to secure the loan — is one of the biggest factors influencing an interest rate.

- A secured loan is backed by an asset, such as property or valuable equipment. Because this reduces the lender’s risk, secured loans typically offer lower interest rates. For our cafe owner example, the new $30,000 coffee machine could potentially be used as security for the loan.

- An unsecured loan does not require a specific asset as collateral. This offers more flexibility for the business owner, but as the lender takes on more risk, the interest rates are generally higher than for a secured loan.

Short-term loans vs. long-term loans

The loan term, or the length of time you have to repay the loan, directly impacts both your regular repayment amount and the total interest you’ll pay.

- A short-term loan, typically with a term of 3 to 12 months, is often used to manage a temporary cash flow gap or fund a small project. While your regular repayments will be higher, the shorter term means you pay less in total interest.

- A long-term loan, which may have a term of several years, is better suited for significant investments like a major fit-out or expansion. The repayments are smaller and more manageable, but you will pay more in total interest over the life of the loan.

Term loans vs. business lines of credit

The structure of the loan also plays a critical role.

- A term loan provides a single lump sum of capital upfront, which you then pay back in regular instalments over a set term. This is ideal for a specific, one-off purchase, like the cafe’s coffee machine in our example.

- A business line of credit provides access to a flexible credit facility up to an approved limit. You can draw down funds as needed and only pay interest on the money you use. This structure is better for managing ongoing or unexpected expenses, such as payroll, fluctuating stock levels, or emergency repairs.

For a more detailed comparison, see our guide on choosing between a business loan vs. a business line of credit.

How your business situation impacts loan costs and options

Every business is unique, and lenders assess a range of factors to understand your specific circumstances. Your trading history, revenue, credit score, and business structure all help a lender to assess risk, which in turn influences the rates and terms you may be offered.

Loan costs for new businesses (trading 6-12 months)

Lenders look for a consistent record of revenue to demonstrate a business’s viability. Because the perceived risk is higher for a newer business, the costs may be different from those offered to a more established company. For a new business with a shorter trading history, this can be a challenge. While some lenders require two years or more of financial records, others specialise in funding newer businesses. Prospa, for example, will lend to businesses that have been trading for 6 months.

The role of your credit score

Your business and personal credit history is a key indicator of financial reliability. A strong credit score, built by paying bills and other debts on time, demonstrates to lenders that you are a dependable borrower. While some lenders have rigid credit score requirements, others can look at your score in combination with your business’s real-time performance to get a more complete picture of your financial health. Generally, a stronger credit history will open up access to more favourable rates.

How business revenue affects your options

The amount of revenue your business generates is a critical factor for lenders. Higher, consistent turnover demonstrates a greater capacity to manage repayments, which can allow you to access larger loan amounts and potentially better terms. Lenders will look at your recent sales history to confirm that your cash flow can comfortably support the loan you’re applying for.

Options for self-employed applicants

For sole traders, demonstrating a stable business income can seem more complex than for a company. Lenders understand this and will typically look at a combination of business bank statements and personal tax returns to assess the financial health of a self-employed applicant. Keeping your bookkeeping organised and your accounts up to date is the best way to present a strong case for your application.

Understanding ‘no credit check’ and ‘low doc’ loans

It’s important to understand what these common marketing terms actually mean for you.

A low doc loan means the lender may accept alternative documents to verify your financial position, such as business bank statements instead of detailed financial reports.

A no credit check offer allows a lender to assess your eligibility using your business’s real-time performance data instead of performing a ‘hard’ credit check that gets recorded on your file. Since multiple hard enquiries in a short time can lower your credit score, these products let you explore your options without any negative impact, which is ideal if you want to compare different lenders or are not yet ready to commit.

Does a faster loan mean a more expensive loan?

There is often a perception that a faster, more convenient application process must come at a higher cost. However, the cost of a loan is determined by the lender’s assessment of risk, not the time it takes to approve an application.

The speed of a loan decision is usually a reflection of the lender’s technology and processes. Traditional lending models often involve manual credit assessments and lengthy paperwork, a process that can take weeks. Modern online lenders instead use technology to securely access and analyse a business’s real-time financial data. This allows them to make a faster credit decision, based on an up-to-date picture of your business’s health. For example, with Prospa you can apply online in minutes and could have funding available in hours.

For a business owner, the more important calculation is often the opportunity cost of waiting. If a slow loan process means you miss out on a time-sensitive opportunity, such as purchasing discounted stock or securing a new contract, the “cheaper” loan could end up being far more expensive in the long run.

“It can take a year to get an overdraft approved and by then the opportunity’s passed. Banks can make you feel bad for needing finance. With Prospa, I barely had to do any research or preparation. It was so easy and I had the funds within a day or two.”

Wondering what your repayments could look like? Get an instant estimate with Prospa Business Loan Calculator