Learn what a low-doc business loan is, how it works, and whether it’s right for your business. Get fast funding with minimal paperwork.

At a glance

- Low-doc business loans give owners faster access to funding by relying on recent bank activity or simple income declarations instead of full financial statements and tax returns.

- They can be used for everything from day-to-day needs like stock, tools, and repairs to larger investments such as equipment upgrades, vehicle purchases, and fit-outs.

- While they offer speed and flexibility, it’s important to understand the costs and repayment obligations so you can choose the right loan for your business.

When you need funding quickly, digging through old records or waiting on accountants can slow everything down. A low-doc business loan cuts out much of that admin, letting you apply with minimal paperwork.

In this guide, you’ll learn how low-doc loans work, what to watch out for, and how low-doc finance options like a Prospa Small Business Loan can support your plans.

What is a low-doc business loan?

A low-doc business loan is a simpler way to access funding without needing full financial statements or years of tax returns. Instead of the detailed paperwork banks often require, lenders use recent bank activity or a basic income declaration to understand how your business is performing.

With online lenders such as Prospa, this can be as straightforward as securely sharing your bank transaction data, confirming your business details and ABN, and completing simple ID checks.

It’s a practical option for sole traders and self-employed owners who may not have lodged recent tax returns or don’t have formal financials ready to go. It can also help businesses with seasonal or irregular income, who may find it difficult to show consistent earnings.

Low-doc loans can also be ideal for newer operators and startups that don’t yet have a long trading history but still need working capital to keep things moving.

How do banks and lenders compare?

Business loan applications can look very different depending on the lender you approach. Some rely heavily on existing customer data or accounting software, while others focus on recent bank activity or manual assessments. When it comes to eligibility, documentation and approval speed, here’s how their low-doc or streamlined pathways seem to compare based on the information provided on their website:

Low-doc business loan options*

| Lender | Lender type | Eligibility | Documentation / process | Decision speed |

|---|---|---|---|---|

| CBA | Major |

ABN. ID. Deposit often required (subject to asset value). Ideal: no arrears in 3 months. No bankruptcy in 5 years. No account collections in 6 months. |

Via NetBank for existing customers. May request extra details (e.g., business plan, projections for <12 months trading). |

Instant for eligible existing customers. Manual, slower review for new customers. |

| ANZ | Major |

ABN/ACN. 6+ months reconciled data. GST registration if turnover >$75k. Turnover <$10m. |

Connects to Xero, MYOB, QuickBooks. | Automated once data is connected. |

| NAB | Major |

ABN/ACN. Requires GST registration. 12+ months trading. Basic ID. |

Connects to Xero, MYOB, QuickBooks. | Automated once data is connected. |

| Judo Bank | Challenger |

ABN/ACN. ID. Trading activity varies by case. |

Application handled via banker call-back. Manual judgement-based assessment. | Case-by-case timing. |

| Moula | Online |

ABN/ACN. 6+ months trading. $10k+ monthly sales. GST registration. |

Online form, link bank or accounting data. | Possible within 24 hours. |

| OnDeck | Online |

12 months trading. $100k+ turnover. 500+ credit score. No prior bankruptcies. |

Online form, link bank data. | Possible within 24 hours. |

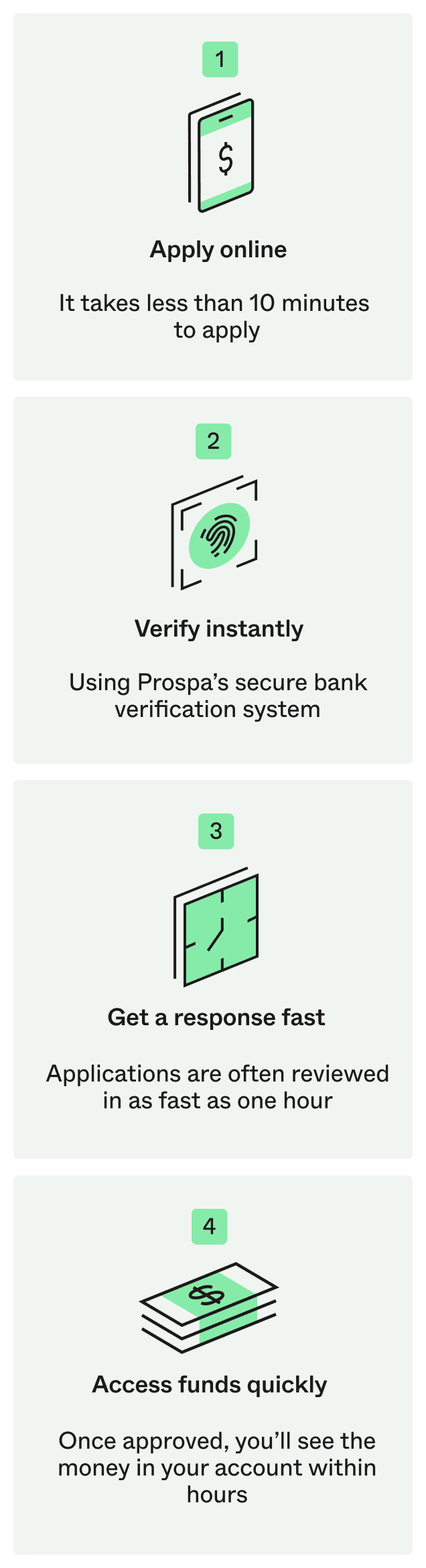

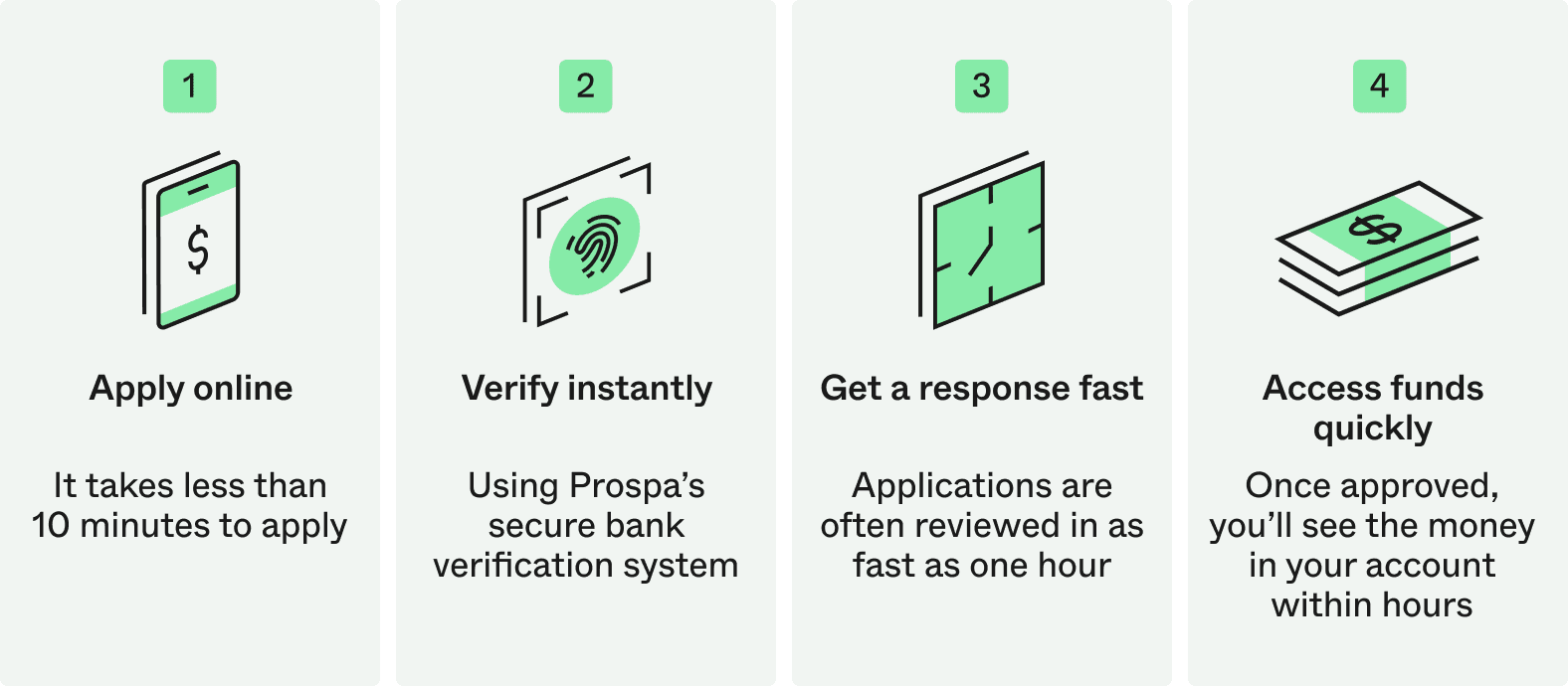

| Prospa | Online | ABN, ID, 18+, recent trading activity. |

Online form, link bank data. Confirm ID, business details, ABN. |

Application in 10 minutes, funding often available within hours. |

*Note: This information is for general reference only and is current as of January 2026. Lender policies are subject to change; please verify the latest details directly with the individual provider.

What can you use low-doc loans for?

Low-doc loans can support everything from your everyday business needs to the larger investments and upgrades that help you take on more work or operate more efficiently. Common uses include:

Day-to-day business needs, such as:

- Replacing tools or small equipment

- Covering repairs or maintenance

- Purchasing stock or materials

- Smoothing short-term cash flow

More significant investments, such as:

- Upgrading major equipment or machinery

- Purchasing or replacing work vehicles

- Installing new software or systems

- Completing fit-outs or expansions

Where the funds are used to buy an asset, depending on the amount you’re borrowing, the lender may require the asset being purchased or other collateral to be used as security.

Let’s say you run a small electrical business and your work van breaks down at the worst possible time. Waiting for tax returns or full financials would delay jobs and impact revenue. A low-doc loan can help you secure the funds needed to replace the van quickly so you can stay on the road and continue taking bookings.

If you’re ready to get started, find out more about how to apply for a Prospa business loan.

What should you watch out for?

Low-doc loans are designed to be simple, but it’s still important to understand the costs and commitments before you move ahead.

- Rates and fees: Costs can vary between lenders depending on their criteria and your level of risk. Being clear on the upfront, ongoing, and potential penalties helps you understand the full cost of borrowing. You can learn more in our guides to interest rates, and fees and charges.

- Repayment obligations: Make sure the repayments align with your cash flow. Stress-test your numbers with some simple scenario planning to see what’s sustainable for your business. Prospa’s business loan calculator can also help you estimate what repayments might look like.

- Early repayment implications: Some lenders apply different fee structures or payout calculations if you repay early, which can have a significant impact. You can weigh up potential benefits and costs in our early repayment guide.

- Accurate documentation: Even with low-doc loans, lenders still need a clear snapshot of how your business is trading. Instead of gathering and uploading PDF statements, Prospa allows you to securely link your business bank account online to provide the required information, and speed up the approval process.

What are the benefits of low-doc business finance?

Low-doc business finance helps you secure funding quickly and stay focused on running your business. Here’s how it can support you:

- Act quickly: Move ahead on opportunities without waiting for full financial statements or extended reviews — ideal for situations where timing matters.

- Preserve cash flow: Spread the cost of purchases over time, keeping cash available for wages, stock, and day-to-day operating expenses.

- Manage variable income: Demonstrate capacity through recent trading activity, which is often enough for businesses with seasonal or uneven revenue.

- Plan with certainty: Maintain visibility over your commitments with set terms and predictable repayments that make future planning easier.

- Verify details instantly: Instead of downloading and printing PDFs, link your business bank account online for a secure, paper-free experience that speeds up the decision process.

Running a business rarely follows a neat financial calendar. When opportunities or disruptions come up before the paperwork is ready, low-doc finance can help you move forward without delays.

If you’re looking for finance that fits your schedule, Prospa’s business loans are a simple, flexible way to get started.