At a glance

- Retailers are under increasing pressure from rising costs, shifting customer habits and cash flow gaps that aren’t always visible in the numbers.

- Simple changes like tightening inventory, planning for seasonal dips and testing new products in small batches can make a big difference.

- With the right tools and funding support, it’s possible to grow your retail business without overextending.

For many small retailers, the rhythm of trading has become harder to predict. Sales patterns are shifting, costs are rising, and cash flow is under more pressure than ever. In the nine months to March 2025, retail insolvencies rose by nearly 20%, reflecting the growing pressure on the sector.

But with the right strategies in place, it’s possible to stay ahead of seasonal dips, avoid cash flow crunches and grow with confidence. This article shares practical tactics tailored to small retail businesses, from inventory planning to low-risk growth ideas, along with tools and funding options to help take the next step.

What makes cash flow so challenging for small retail businesses

Retailers are facing a unique combination of pressures that make cash flow harder to manage than ever. “The convergence of online retail growth, soaring rental costs and changing consumer behaviours has created a perfect storm for small businesses,” said Mark Pizzacalla, partner at BDO.

For many, this is showing up in reduced foot traffic, rising operating costs and customers choosing shopping centres over local strip stores. Even retailers with loyal customers and steady sales can find it difficult to stay ahead of their financial obligations.

Cash flow gaps often stay hidden in the day-to-day running of a store. A solid sales month doesn’t always mean things are running smoothly. Stock may be sitting unsold, or wholesale payments may still be pending. Common pain points include:

- Capital tied up in slow-moving inventory

- Late customer payments disrupting cash cycles

- Margin pressure from rising supplier and staffing costs

When pressure builds on multiple fronts, cash flow shapes every decision: what to stock, when to restock, how to staff and whether the business is in a position to grow.

Cash flow strategies every small retailer should be using

Right now, many small retailers are feeling the strain. Inventory costs are rising, customers are more cautious, and promotional activity is becoming more expensive to sustain.

According to BDO national retail leader Salim Biskri, many small businesses are operating with limited working capital while also facing longer payment cycles from customers. It’s a combination that can quickly disrupt cash flow.

Practical, smart tips for managing retail cash flow, planning for seasonal dips and funding growth without overextending your business.

Staying in control means knowing where cash is tied up and adjusting operations early to protect it.

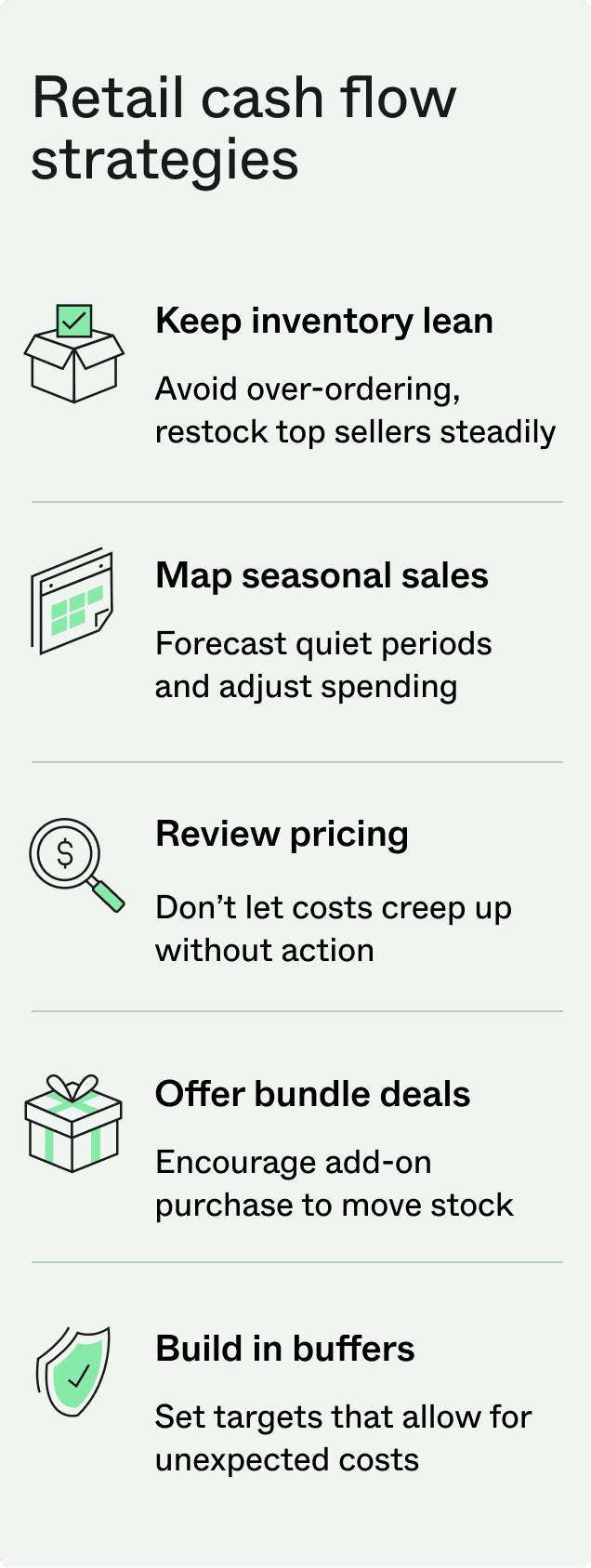

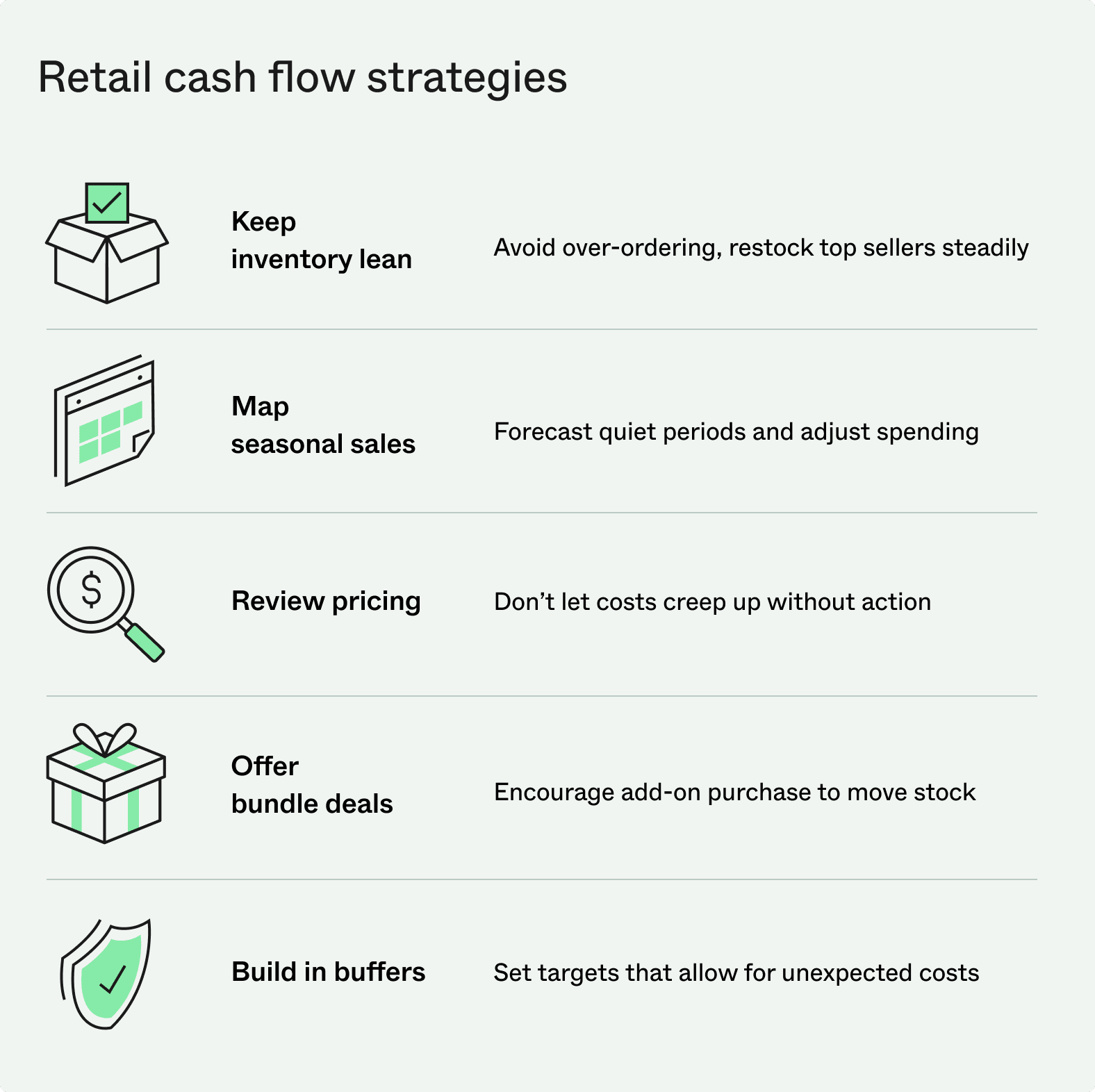

Here are six strategies every small retailer should consider:

1. Keep inventory lean and responsive

Avoid over-ordering or tying up cash in stock that doesn’t move. Use POS data or sales reports to identify your top performers, and restock only when those items are trending steadily. Trial small volumes before committing to new products.

2. Map seasonal sales patterns in advance

Don’t wait for quiet periods to impact cash flow. Review previous years’ sales by month and overlay any known events or upcoming campaigns. Use a simple spreadsheet or forecasting tool to adjust inventory orders, staffing and marketing spend before sales dip.

3. Review pricing and margins regularly

Even small cost increases from suppliers can eat into your margins over time. Revisit your pricing at least quarterly, especially for bestsellers. Consider adding low-cost value such as free gift wrap or samples to justify price adjustments without discounting.

4. Refine your retail store strategy

Where and how products are displayed can affect both turnover and cash flow. Make high-margin or high-demand items more visible, and update displays regularly to reflect seasonal changes or sales trends.

5. Use bundle offers or small incentives to move stock

Rather than relying on blanket sales, group slow-moving items with popular ones or offer a gift-with-purchase to shift excess inventory. Tools like Shopify’s bundle apps or in-store POS promotions make this easy to roll out.

6. Build in cash flow buffers wherever possible

When setting your monthly targets, include a cushion for late payments, surprise costs or delays in inventory delivery. A basic four to six week rolling forecast, even in Excel, can help you spot shortfalls before they happen. You can also create a simple cash reserve to give your business more breathing room when things are quiet or unpredictable.

Growth strategies that won’t put your cash flow at risk

Once cash flow is under control, growth becomes the next focus. But that doesn’t mean doubling down on spend. The most effective retail business strategies rely on improving margins, extending reach or strengthening customer relationships without draining resources.

Here’s how to grow sustainably:

- Trial new products in limited runs. Instead of rolling out an entire collection, start with a handful of SKUs and track how they perform. Sales data and customer feedback will tell you what’s worth scaling without tying up capital in slow movers.

- Team up with a local brand. It could be as simple as a bookshop working with a local café, or a gift store showcasing handmade ceramics from a nearby maker. Collaborations like these can help you attract new customers, offer more value and even share marketing costs.

- Keep your marketing simple and consistent. Highlight new products or local collaborations through email, social media or in-store signage. These small, steady efforts are often the most effective retail marketing strategies for small businesses.

- Use your checkout to drive more value. Whether in-store or online, small add-ons at the point of sale can lift the average order size. Train staff to suggest related items, or use your ecommerce platform to recommend bundles based on browsing or purchase history.

- Start selling online in a focused way. You don’t need a full ecommerce operation to reach more customers. A simple online store, curated product set or marketplace presence can help you generate extra sales without overstretching. If you’re not sure where to begin, these ecommerce strategies can help you take the first step.

- Give regulars a reason to come back. Retention doesn’t always need a loyalty program. Surprise-and-delight moments or spontaneous gestures that make the experience feel personal often outperform generic loyalty offers.

When funding makes sense for retailers

Even the most disciplined retailers can hit a point where cash flow alone isn’t enough to support growth. A short-term gap, a seasonal spike or an opportunity that needs upfront investment might call for extra support. The right funding solution, combined with practical tools, can help bridge the gap without putting the business under pressure.

Here’s what to consider before seeking additional funds:

- Know what you need and why. Maybe you’re preparing for a peak season, planning a small fit-out or covering the upfront cost of a new product range. Clarity around the numbers and intended use of funds helps you stay focused and make confident decisions.

- Choose the right type of funding. A short-term retail business loan might be right for one-off investments or supplier payments. For more flexible access to funds, a Prospa Line of Credit gives you ongoing access up to your approved limit, so you can draw down what you need, when you need it.

- Check how the repayments fit your cash cycle. Consider how repayments will affect your regular cash flow. If your income fluctuates, look at options that give you breathing room during slower months, or align more closely with your sales pattern.

- Use tools that give you visibility. Before applying for funding, take stock of where your business stands. The Prospa Loan Calculator can help you estimate repayment amounts and explore what different funding scenarios might look like.

- Ask questions and compare options. Not all retailer funding solutions are created equal. Look at cost, flexibility, approval speed and the level of support available.

Want to talk it through? Speak to a Prospa specialist about what’s possible for your retail business.