Release date: 24 February 2023

Prospa Group Limited (ASX:PGL) (“Prospa” or the “Company” or the “Group”) is pleased to announce its financial results for the half year ending 31 December 2022 (“H1 FY23”).

The Company has demonstrated strong growth in cash and profit metrics; while strategically investing in new products and technology to support long term growth and increasing its loan loss provision as cash rate rises continue and economic growth is expected to slow.

H1 FY23 highlights were also outlined in the trading update released to the market on 13 February 2023 (“Trading Update”). The Trading Update can be accessed via the Prospa Investor Centre (https://investor.prospa.com/investor-centre/) or the ASX website.

H1 FY23 Group highlights

- Total Originations1 of $425.5 million, up 35.1% on the prior corresponding period (“pcp”) (H1 FY22: $314.9 million).

- Closing gross loans increased to $855.8 million, up 66.3% on pcp (H1 FY22: $514.6 million).

- Revenue2 reached $135.3 million, a 72.4% increase on pcp (H1 FY22: $78.5 million).

- Active customers grew to 19,900, an increase of ~1,900 from the previous quarter (Q1 FY23).

- Operating cashflow increased to $47.0 million, up a significant 98.0% from pcp (H1 FY22: $23.7 million).

Greg Moshal, Co-Founder and Chief Executive Officer said:

“I’m pleased by Prospa’s strong momentum, which is underpinned by our mission to be the financial partner of choice to small businesses in Australia and New Zealand. We have continued to invest in our products and technology so our customers have simple, stress-free, and seamless financial management tools, and they can focus on what they do best. Despite this increased investment, Prospa still posted an EBITDA profit for the half.

“The impacts of inflation, rising rates and a tight labour market have increased uncertainty in the operating environments for many small businesses. We are seeing stress in some of our lower risk grades and have revised our commercial credit risk assessment policies in-line with these changing conditions. Notwithstanding the macro environment and tightening credit, we continue to grow our business by meeting customer demand, building out our product roadmap, and applying a strong focus on our portfolio management settings.”

Ross Aucutt, Chief Financial Officer said:

“Our strong underlying performance continues despite emerging challenging economic conditions across Australia and New Zealand. Prospa’s business model continues to be highly cash generative even with significant investment in our products and technology platform. We are in an interesting situation where our total cash balance was $125 million, exceeding our market capitalisation of $100 million as of 31 December 2022 by almost 25%.

“Capital management remains a core focus for our business. The Company continues to invest in its technology, new product development and growth. We apply a prudent approach to our loan book through the dynamic management of risk and commercial settings and we’ve been able to successfully pass through a small percentage of the cost of funds increases without dampening demand while retaining a stable NIM.”

Outlook

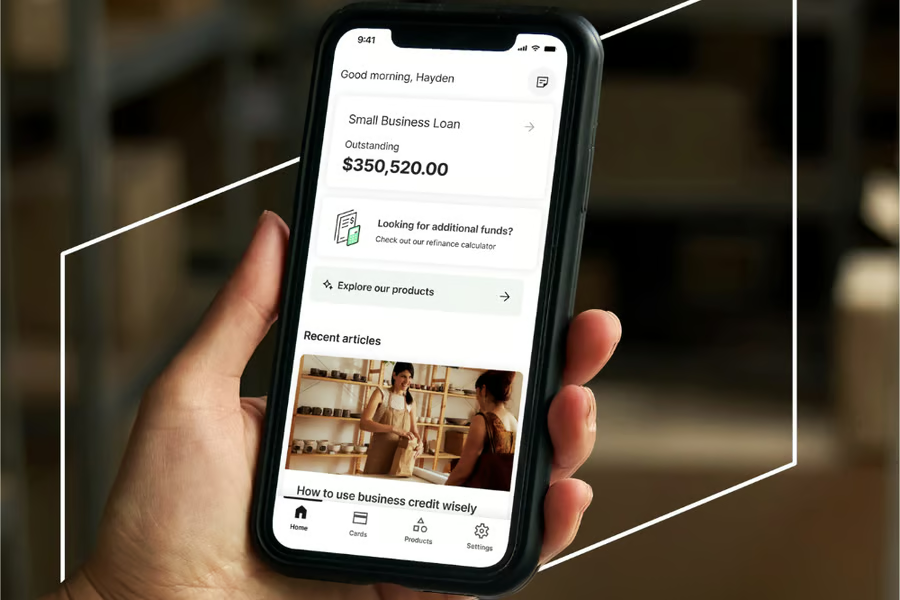

The Company remains focused on maintaining its position as the premier online lender to small business while delivering profitable growth. Customers remain at the core of Prospa’s focus. In August 2022, the Company launched a new mobile application to improve customers’ experience, further adding to its innovative digital cash flow management tools. The new application provides customers with a single view of their balance for all Prospa credit products, including the recently launched Business Account with a VISA business debit card and Overdraft that has been offered to a pilot cohort of customers. This new product suite enables customers to better understand and manage their business cash flow, to grow, run, and pay anywhere, anytime.

This new wave of financial and transactional products coupled with the Company’s recent rebranding, positions it well into the future as it meets a greater set of customer needs.

Footnotes:

- All references to Originations in this document are from all sources, including Small Business Loan, Business Line of Credit (including undrawn amounts), Back to Business Loan, Back to Business Line (including undrawn amounts) in Australia and New Zealand. Small retrospective changes in origination figures may occur as result of back dated cancellations or modifications to support customer outcomes. All figures are expressed in AUD terms unless otherwise specified.

- All references to Revenue in this document represent Total income before transaction costs.

- 1H22 operating cash flows have been updated to align with the Group’s revised presentation of cash flows from loan origination fees. This has resulted in a $1.6m decrease in net cash from operating activities.

ENDS

For further information, contact:

Melanie Singh

Senior Investor Relations Manager, NWR

[email protected]

+61 439 748 819

About Prospa

Prospa Group Limited (ASX: PGL) is a leading fintech with a commitment to unleash the potential of every small business in Australia and New Zealand. We do this through an innovative approach to developing simple, stress free and seamless financial management products and services.

Since 2012, we have provided more than $3 billion of funding to support the growth and operations of thousands of small businesses. We also work with more than 12,000 trusted brokers, accountants, and aggregator partners, to deliver flexible funding solutions to their clients.

At Prospa, we're serious about our impact on our people, communities, and the planet. Our core company value of One Team is backed by our recognition as a Great Place To Work in Australia and a WORK180 Endorsed Employer for Women.

For more information about Prospa, visit prospa.com or investor.prospa.com.