FY22 Group highlights:

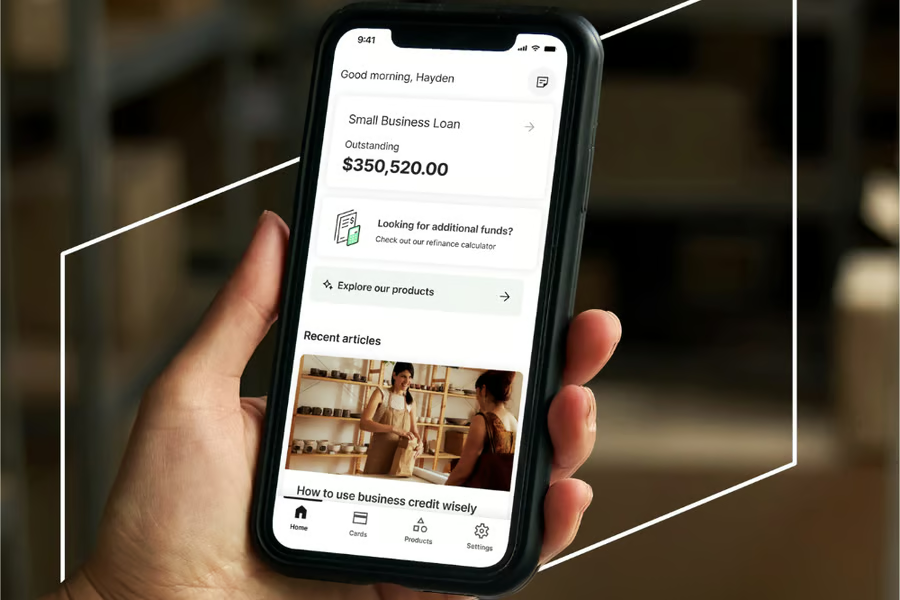

- Our new technology platform created substantial value and opportunities across all products, including the launch of the New Zealand Line of Credit.

- Strong performance across all metrics resulted in profitability, with EBITDA [1] increasing to $12.1 million, a 2274% increase on the prior corresponding period (“pcp”) (FY21 $0.5 million).

- Originations increased to $732.8 million, up 52% on pcp (FY21: $483.4 million), with June 2022 recording the highest month on record at $104.6 million.

- Closing gross loans increased to $701.3 million, up 64% on pcp (30 June 2021: $427.1 million), driven by continued credit demand from small businesses.

- Revenue [2] for the period reached $178.3 million, a 51% increase on pcp (FY21: $117.7 million).

- Promising start to FY23, with $66.0 million in originations recorded for July 2022 during a seasonally slower period (July 2021: $41.8 million).

- Stable credit quality within the loan book, strong margins, a lower cost of funds and improving operating leverage underpinning the business in a rising rate environment.

Prospa Group Limited (ASX:PGL) (“Prospa” or the “Company” or the “Group”) is pleased to provide its full year results for the 12 months ended 30 June 2022 (“FY22”).

FY22 financial highlights

Prospa delivered a record-breaking year for originations, reaching $732.8 million, up 52% on pcp (FY21: $483.4 million). In the month of June 2022 alone the Company also achieved its highest ever month of $104.6 million in originations. The performance throughout the year demonstrates the strength of Prospa’s business model, and continued investment in core technology.

The New Zealand business continues to go from strength to strength, with originations contributing AU$122.9 million over the period (16.8% of total originations). This highlights the growing awareness of the Prospa brand, further enhanced by the launch of Line of Credit.

As a result of strong demand for credit, closing gross loans reached an all-time high of $701.3 million, an increase of 64% on pcp (30 June 2021: $427.1 million).

Total revenue increased by 51% for the period to $178.3 million (FY21: $117.7 million), supporting the uplift in realised portfolio yield [3] to 34.1% (30 June 2021: 32.7%).

The Company’s investment in further developing its technology platform and delivering on its growth strategy resulted in achieving a significant uplift in EBITDA of 2274% to $12.1 million.

Prospa delivered strong growth in conjunction with an overall improvement in the credit quality of the loan book compared to FY21. In a rising rate environment, the Group pleasingly maintained an attractive Net Interest Margin (“NIM”) of 29.6% for FY22, up from 27.7% in FY21. The NIM performance was supported by increases in yield and a reduction in funding costs which decreased by 0.9 percentage points to 5.0% in FY22. The Company expects improved funding margins will partially offset base interest rate increases.

During the year, Prospa further diversified funding sources with its first public asset-backed securitisation (“ABS”) of $200 million. As of 30 June 2022, the Company had $702.0 million of available third-party facilities, up from $458.6 million as of 30 June 2021.

To aid growth in FY23, the Company expanded its Propela Trust facility by $67.5 million, increasing Prospa’s undrawn capacity to $126.6 million as of 31 July 2022.

Overall credit provisioning reduced to 7.2% in FY22, down from 7.9%. As macroeconomic conditions remain uncertain, Prospa continues to focus on the credit quality of the loan book.

Greg Moshal, Co-Founder and Chief Executive Officer, said:

“It has been an incredible year, with the team investing a tremendous amount of time and effort to deliver these results. It’s a great way to celebrate Prospa’s 10-year anniversary.

“Our continued investments and preparation ensured we were well positioned to service more customers during a time of high demand for funds amongst small business owners across Australia and New Zealand. The hard work of each team member helped the business repeatedly break records, and these efforts were combined with determination to deliver innovative products to simplify cash flow management for our customers. The fruits of their efforts have been apparent with the successful launch of our new credit solutions, and Prospa’s business account, now available to small business owners from August 2022.”

Ross Aucutt, Chief Financial Officer, said:

“Prospa delivered powerful growth while simultaneously investing in the business for future years. Our performance was delivered while maintaining the credit quality of the loan book within the board mandated static loss range of 4% – 6%.

“EBITDA performance was meaningfully higher than in FY21. The business generated significant operating cash flow that funded investments in our technology platforms. In addition, we have continued to be innovative in accessing diversified funding sources and pleased to see our cost of funds reduce by 0.9 percentage points since FY21. These results highlight the strength of Prospa’s business model and its competitive advantage in the fintech lending space.

“FY23 has started well with July originations at $66 million, up 58% on July 2021.”

Operational highlights

Prospa’s unique technology underpinned the robust performance over the period. The Company invested to enhance core technology to scale existing lending products, including the successful launch of Prospa Plus Business Loans to offer up to $1,000,000 and the New Zealand Line of Credit with a facility of up to NZ$150,000.

The Company continues to deliver innovative digital cash flow management tools, and after a successful trial with existing customers, Prospa’s Business Account and Visa debit card are now available to small businesses across Australia.

To further improve the customer experience for those engaging with Prospa’s product, a new mobile app launched in August 2022. The new app provides customers with a single view of all their Prospa products, including credit, and the recently launched business account.

Furthermore, the technology improvements helped boost operational efficiencies to drive faster credit decisions. These enhancements leveraged deep insights and data, assisting the growth in total active customers to over 16,000, while maintaining the Net Promoter Score of 80+[4]. The agility of Prospa’s platform allows adjustments to risk settings to rapidly target specific customer types and optimise financial outcomes. Prospa expects to remain within the Board mandated static loss rate range of 4-6%.

Outlook and strategic priorities

Prospa remains focused in maintaining its position as the leading online lender to small businesses, while expanding its financial solutions to assist customers to manage their cash flow.

Over FY23, the Company plans to release new features in the All-In-One Business Account such as BillPay, overdrafts, foreign exchange, and invoicing, to enable small business owners to better manage their cash flow within one single platform. Over time, this is expected to increase retention and improve customer lifetime value.

Greg Moshal added:

“Our strong performance highlights the Company’s ability to execute. While uncertain economic conditions prevail, we will continue to develop on our robust foundations through the investment in technology to further strengthen our business and deliver sustained growth.

“We’re excited about the year ahead, with the team focused on delivering the next growth phase to support small businesses. The Company is well positioned to deliver another set of strong results. We will keep the market informed about our range of new products to drive greater engagement with customers and offer increased lifetime value, while remaining well ahead of the curve amongst our competitors.”

Webcast

Prospa Group CEO Greg Moshal, CFO Ross Aucutt and CRO Beau Bertoli will present the Company’s full year results at 10:30am today, Thursday 25 August 2022. To register for the webcast, please click here.

This announcement has been authorised for release by the Board.

For further information, contact:

Company Secretary

Ross Aucutt

CFO and Interim Company Secretary

Email: [email protected]

Media & Investor Relations

e: [email protected]

1 All references to EBITDA in this document represent Earnings before interest on lease liabilities, tax, depreciation and amortisation and share-based payments.

2 All references to Revenue in this document represent Total income before transaction costs.

3 All references to Realised portfolio yield in this document represent the interest (excluding transaction costs) and fee income earned during the period on the average portfolio balance during the respective period, annualised.

4 Net Promoter Score was in excess of 80 for the period 1 April 2022 to 30 June 2022.