Finish the year strong and start the next with purpose. Discover practical ways to tidy your finances, set strong financial goals, and use cashflow strategies and business loans to grow your business in the year ahead.

At a glance

- Reviewing your finances before the year ends helps you identify what’s working, what needs attention, allowing you to set realistic goals to grow your business.

- Simple actions like chasing invoices, creating promotions, and revisiting supplier terms can free up cash and create early momentum for the new year.

- Understanding your funding options ensures you can be ready to act quickly when opportunities arise.

As the calendar year winds down, most business owners are ramping up for one of their busiest periods, juggling orders and sales, keeping the lights on and the team organised. It might feel like the worst time to plan; but waiting until the new year means you’re already reacting, not planning. Taking time now to review your position and plan your goals ahead ensures your business enters the year prepared and ready for growth.

From tidying up your finances and building early momentum, to exploring the funding tools that can support long-term growth, this guide covers the practical steps you can use to start the year strong and focused on your goals.

Why year-end financial planning matters

When you are deep in day-to-day operations, it’s easy to confuse ‘being busy’ with ‘being on track’. A year-end review is an ideal chance to get out of the engine room and understand what’s really working and what needs attention.

Without it, you risk flying blind. Small issues can carry over and get worse. You might get hit with a surprise tax bill in March or keep pouring money into a marketing channel that isn’t working. This is your chance to stop reacting and start planning. By checking cashflow, forecasting for seasonal changes, and reviewing your financial position now, you can set realistic targets that support growth instead of just keeping things running.

Set clear financial goals

Once you have a full picture of where your business stands, it’s time to set direction for the year ahead. For a goal to be effective, it needs to be clear, measurable, realistic, and linked to your broader strategy — all with a clear time frame for review.

A mix of short-term goals (like improving cashflow or managing costs) and long-term goals (like increasing profitability or expanding into new markets) will help balance immediate needs with future growth.

Here are some examples to get you started:

- Improve cashflow: Reduce average payment times by 20% or build a cash buffer equal to one month’s expenses.

- Increase revenue: Lift monthly sales by 10% through repeat customers or new marketing campaigns.

- Reduce operating costs: Cut ongoing expenses by 5% by renegotiating supplier terms or cancelling low-value subscriptions.

- Manage debt: Pay down 10% of existing business debt while maintaining enough cash for day-to-day operations.

- Invest in growth: Allocate funds toward one major upgrade, such as new equipment, a digital system, or staff training that supports long-term capacity.

Remember that specific targets are not arbitrary. Base them on your business history and upcoming plans, for example, past profit trends, expected seasonal demand, or new product launches. Setting relevant and measurable goals like these keeps you accountable and helps track progress.

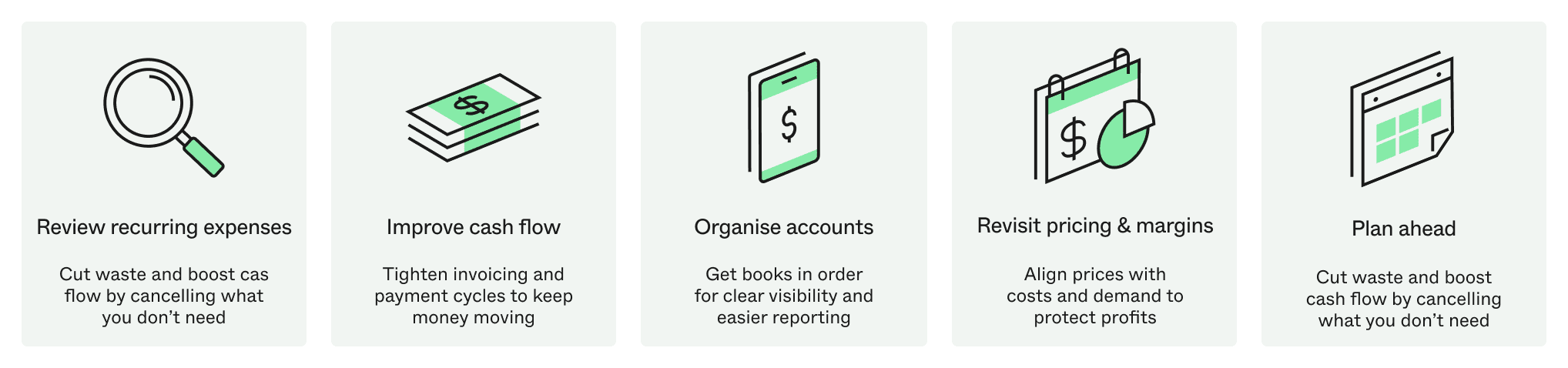

Practical tips to tidy up your finances

With your goals in place, it’s time to make sure your finances can support them. Organise and strengthen your base by tightening processes, cutting waste, and getting visibility of key information.

Here’s where to focus:

- Review recurring expenses: Go through recurring costs and cancel what’s no longer adding value. Even small savings each month can make a difference to your cashflow.

- Improve your cashflow: Check your invoicing cycles and payment terms to ensure you have cash on hand when it’s time to pay wages, suppliers, and bills.

- Organise bookkeeping and accounts: Make sure all invoices, receipts, and statements are up to date before the new year. Clean books make tax preparation easier and give you a clearer view of performance.

- Revisit pricing and profit margins: Check that your prices still reflect costs and market demand. Small adjustments here can protect profits and help you weather future slumps.

- Plan for upcoming expenses: Map out predictable costs like rent, salaries, and bills to understand your cashflow, so you can manage outflows and avoid surprises.

Tidy up your finances

Tidying up your finances now gives you a solid foundation for the year ahead, and more time to focus on the opportunities that come with it. Learn how a business account can help you streamline this process.

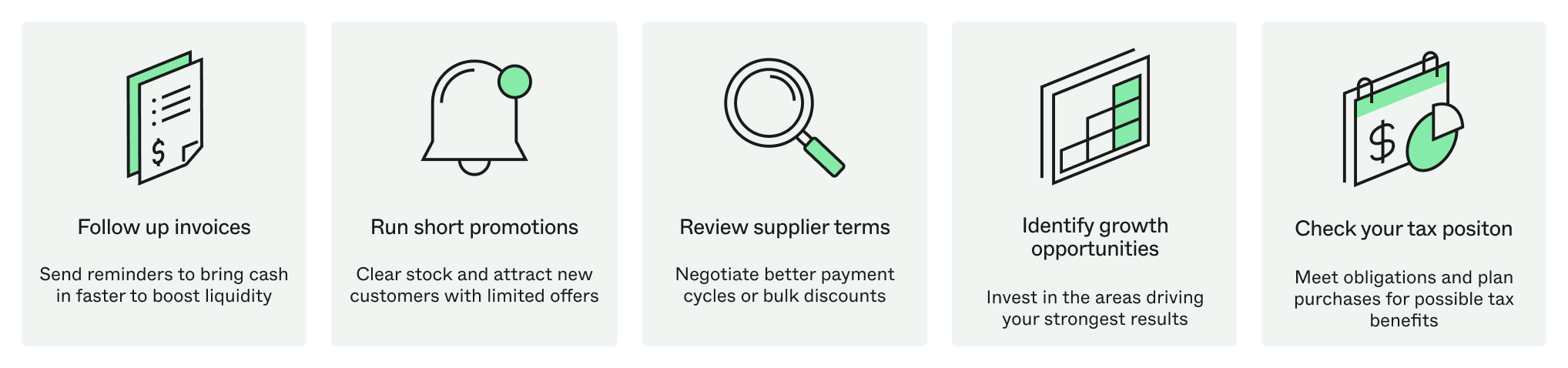

Quick wins to start the new year strong

Once your finances are in order, it’s time to build momentum. A few quick actions now can create early wins and set a positive tone for the months ahead.

Try these simple steps:

- Follow up on outstanding invoices: Send a quick reminder or offer flexible payment options, such as instalments or early payment discounts.

- Offer limited-time promotions: If you’re in retail or hospitality, a short, focused offer can help clear stock and attract new customers.

- Revisit supplier terms: Negotiating better payment cycles or bulk discounts can give you more breathing room in early cashflow.

- Identify fast-growth opportunities: Look at products or services that performed well this year and plan how to double down on that success.

- Check your tax position: Make sure obligations are met and consider whether any end-of-year purchases could deliver tax advantages.

Start the new year strong

Leveraging financial products for growth

Strong financial planning is also about knowing your options before you need them. Whether you’re managing a short-term cashflow gap, investing in equipment, or taking advantage of a growth opportunity that can’t wait, the right funding solution helps you act quickly without putting pressure on day-to-day operations.

A business line of credit can be a flexible option for covering short-term needs, giving you access to funds as you need them, rather than taking out a lump sum. For larger investments, a small business loan or Prospa Business Loan Plus for funding amounts over $500K can provide the capital to expand, buy new equipment, or launch a new product line.

Not sure which approach fits your goals? Our guide on choosing the right funding outlines how each product works and what to consider.

|

“Prospa’s application process was so quick and the staff were amazing to deal with.” – Brad Day, Café Owner |

|---|

Get your business ready for what’s next

A new year brings the opportunity to reset and plan ahead. By setting clear goals, strengthening your financial position, and exploring funding options that fit your needs, you can start the year focused, prepared, and ready to grow.

With options tailored for different stages of business growth, Prospa’s range of loans can help you start the new year strong.