Worried your credit score isn’t “good enough” for a small business loan? Here’s what really matters to lenders and how you can put your best application forward.

At a glance

- Most lenders in Australia look for a credit score of at least 600, but non-bank lenders often consider scores from 400.

- Lenders also assess overall business health, including cash flow, trading history, and financial records; which can outweigh a lower score.

- By analysing turnover, cash flow, and hundreds of other data points, alternative lenders look beyond your credit history to give small businesses with potential a genuine path to funding.

You already know your credit score matters when applying for a small business loan, but right now, some big questions are circling in your mind: Is my score high enough? What if it’s lower than I’d like? Will applying hurt it even more?

It’s natural to worry that one number could make or break your chances, especially when you’re ready to move forward and don’t want an application to stall your plans. A recent Equifax report shows small business credit applications rose 1.6% year-on-year in Q1 2025, highlighting growing demand for funding.

But while your score is important, alternative lenders look at the bigger picture, including cash flow, trading history, and repayment behaviour, to give you a fairer, more balanced assessment. That means you may still have options, even if your small business loan credit score isn’t perfect.

What credit score do lenders typically look for?

When you’re researching small business loans, one of the first questions that comes up is what credit score you actually need to get approved. In Australia, while many traditional lenders set a threshold of around, requirements are often more flexible with non-bank lenders, who may consider scores from as low as 400.

Regardless of the lender, scores above 650–680 are generally preferred, and anything over 700 is usually classed as “very good,” giving you the best chance of fast approval, lower interest rates, and access to a wider range of loan options.

Here’s how credit score ranges typically break down across major reporting agencies:

Credit score ratings by major reporting agency

| Score | Equifax | Experian | illion |

|---|---|---|---|

| Excellent | 853-1200 | 800-1000 | 800-1000 |

| Very Good | 735-852 | 700-799 | 700-799 |

| Good | 661-734 | 625-699 | 500-699 |

| Average/Fair | 460-660 | 550-624 | 300-499 |

| Below Average | 0-459 | 0-549 | 1-299 |

While most lenders rely on reports from Equifax, Experian or illion, some also check CreditorWatch, which uses a different rating scale. Instead of numbers, it grades businesses from A1 (very high credit quality) down to F (default).

CreditorWatch credit score ratings

| Grading | Risk Level | Typical Loan Access |

|---|---|---|

| A1 – A3 | Very high | Best access, lowest rates |

| B1 – B2 | High | Good access, competitive rates |

| B3 – C1 | Good | Moderate access, standard rates |

| C2 | Average | Limited options, higher rates |

| C3 | Below average | Hard to obtain, costly |

| D1 – D3 | Poor | Rarely approved |

| E – F | Impaired/default | Typically ineligible |

Most traditional lenders prefer businesses in the A or B range, which often equates to an Equifax score above 700 or “Good” on Experian/illion. If your business is graded at C2 or lower, funding can become much harder to secure — or come with higher costs. That’s why keeping an eye on your standing across all credit reporting agencies is important.

Not sure where you stand? Use this simple guide to see how lenders may view your score:

- 700+: Strong position for approval, best rates, and widest options.

- 650–680: Often acceptable, though terms may vary.

- 600–649: Minimum range for many lenders — approval is possible but may come with higher costs.

- Below 600: Considered higher risk; you may need to show strong cash flow or explore alternative loan options.

Why your business’s overall health matters more than a single number

Your credit score is one piece of the puzzle, but it’s far from the only thing lenders look at when deciding to approve a small business loan. In Australia, lenders assess the overall health of your business. That means your trading history, revenue, cash flow, financial records, and even your business plan all matter just as much as the score itself.

Take an example: imagine a local specialty coffee roaster that’s been trading for 18 months. The owner has built a loyal customer base of cafés, shows consistent monthly revenue above $15,000, and can provide clean BAS statements and healthy bank records.

Even if their personal credit score is just “average,” a lender may still approve funding because the business itself demonstrates stability, positive cash flow, and a clear plan for growth.

Key eligibility factors lenders typically assess include:

Trading history

Most lenders want to see that your business has been operating for at least 6–12 months. This proves you’ve established regular operations and can weather normal ups and downs. For larger loans, some lenders may look for two to three years of history.

Revenue and turnover

A minimum monthly turnover of around $5,000–$6,000 is often required for unsecured loans. For bigger amounts, such as loans over $150,000, annual turnover above $1 million is preferred to show your business can handle larger repayments.

Cash flow

Healthy, consistent cash flow is one of the strongest signals a lender looks for. They’ll review bank statements, profit and loss reports, and BAS to confirm you can comfortably cover loan repayments on top of existing expenses.

Financial statements

Having at least one year of accountant-prepared financials, business tax returns, and BAS filings gives lenders confidence in the accuracy of your numbers. Strong documentation can speed up the approval process.

Business structure and ownership

To qualify, you’ll need a valid ABN or ACN, and the small business owners must be over 18 and Australian citizens or permanent residents. These requirements establish that your business is formally registered and legally eligible.

Business plan and forecasts

For new businesses or those planning to expand, lenders often want to see a realistic plan for the future. A clear outline of how funds will be used, along with income projections, helps prove your small business is viable and ready for growth.

By showing strength across these areas, you demonstrate to lenders that your business is resilient and capable of repaying a loan, which can sometimes outweigh a middling credit score.

Pro tip: Staying on top of your BAS and ATO obligations shows lenders that your finances are well managed. Missed or overdue tax payments can raise red flags during an application, even if your revenue and cash flow look strong. Keeping everything up to date gives you a smoother path to approval and helps protect your business credit profile.

A Prospa Business Line of Credit gave PUPSTYLE founders Tatum and Adam Ioannidis the flexibility to keep scaling their luxury dog accessories brand. After tripling revenue in just a year, they wanted the confidence of having funds available for future opportunities without committing to a fixed loan amount.

“It was such peace of mind to have funds approved that we can draw down when we need to. It helps with cash flow as we grow our ecommerce store and invest in more marketing. The application process was so simple I can barely remember it. All I know is that it was quick and easy.”

Prospa’s support helped PUPSTYLE seize opportunities they might otherwise have missed, fuelling sales growth of more than 200% in just one year.

Can you get a small business loan with a bad credit history?

If you’ve struggled with your credit in the past, or you haven’t built up much of a credit history yet, it’s easy to feel like getting a small business loan will be out of reach. You might have already even Googled or AI searched for “how to qualify for bad credit business loans” or wondered if no credit check business loans even exist.

The reality is, while a poor score can narrow your choices, it doesn’t necessarily shut the door. That’s because lenders like Prospa assess more than just your credit history.

Prospa’s complex credit assessment tool reviews over 450 data points from sources such as your bank statements, BAS, and verified government records. It looks at how your business is performing today: things like your turnover, cash flow, and trading history; alongside your personal credit profile. This means that even if your score is lower than you’d like, strong revenue and consistent cash flow can still work in your favour.

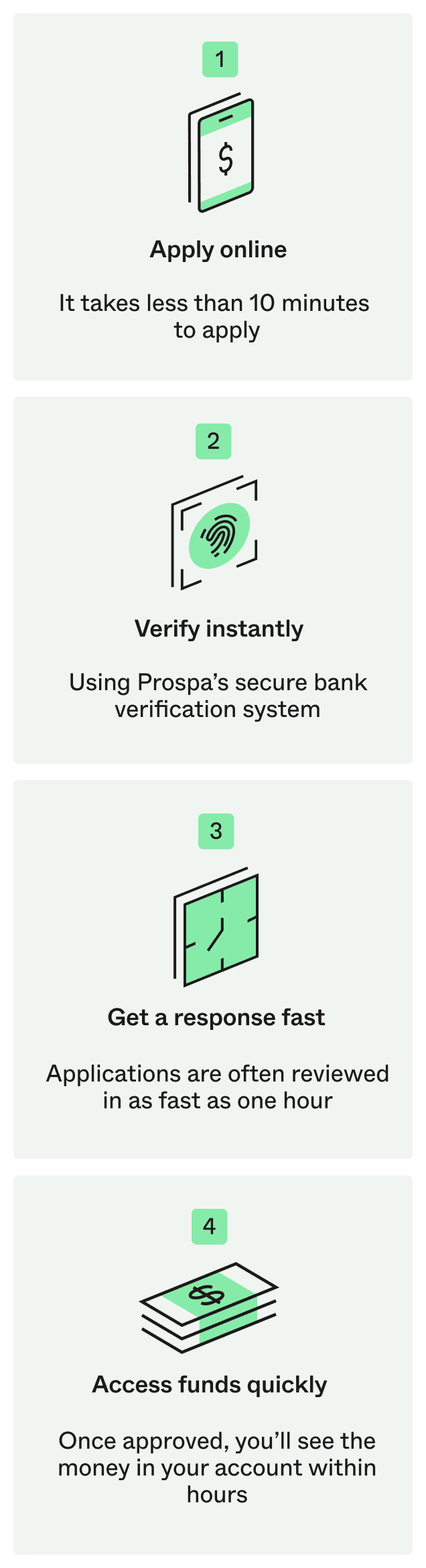

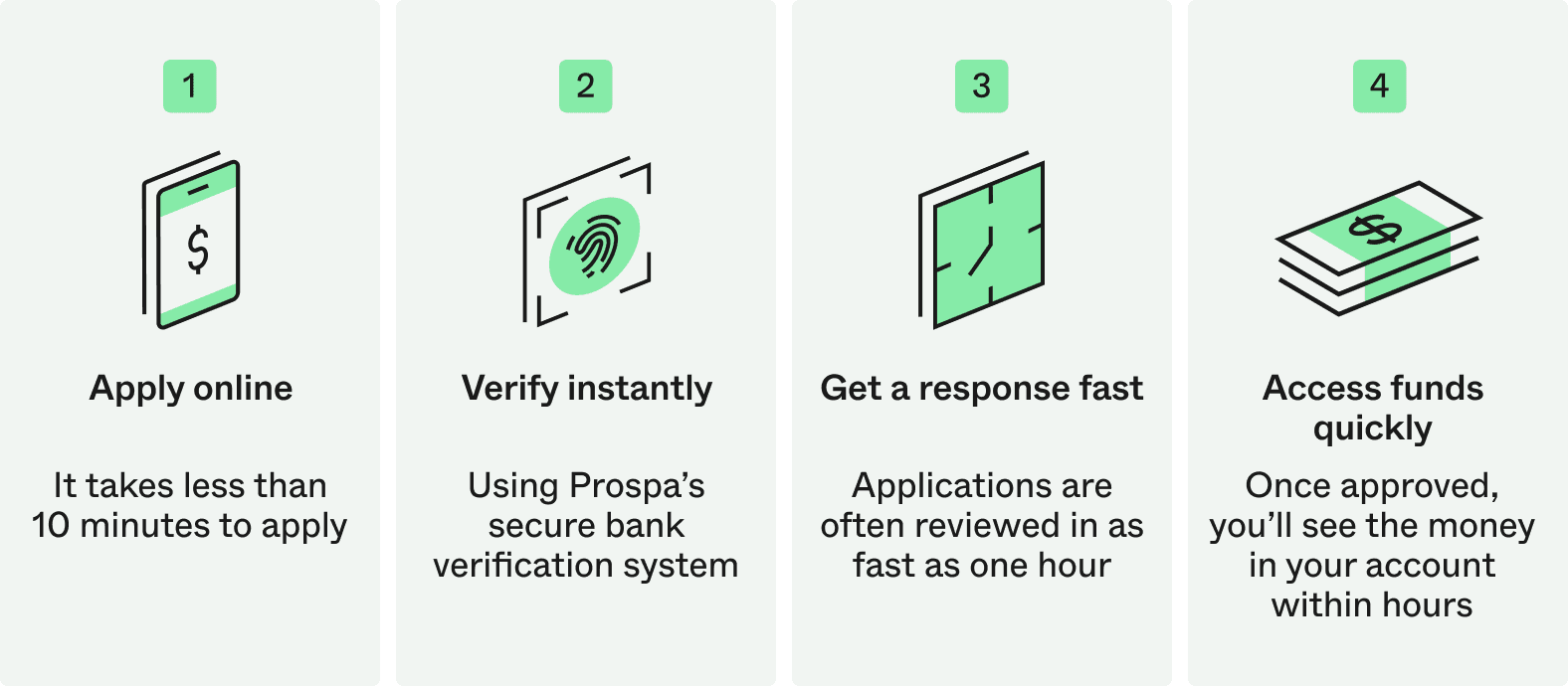

The application process is built for speed and simplicity:

- Apply online in under 10 minutes. All you need are basic details such as your ABN and driver’s licence, plus access to your business bank statements.

- Verify instantly. Using Prospa’s secure bank verification system, your statements are checked on the spot — so you don’t have to upload endless paperwork.

- Get a decision fast. Many applications are reviewed within hours, often as fast as one hour.

- Access funds quickly. Once approved, the money can be in your account within hours of settlement.

Prospa application process

For smaller amounts (up to $150,000), Prospa doesn’t require upfront security, making it easier for businesses with a thin or challenged credit profile to access funding. And if you want to see what repayments might look like before applying, you can use the Prospa Business Loan Calculator to run the numbers.

The bottom line: Even with a bad credit history or no established score, you may still have options. If your business is showing healthy signs of growth and stability, Prospa’s broader approach could give you the chance to access finance when you need it.

How to check and strengthen your credit profile

Before applying for finance, it’s worth running a business credit check in Australia to see how your business is viewed by lenders. You can do this online through providers like Equifax, illion, Experian, or CreditorWatch. Each offers simple sign-ups, and in most cases you can access your report for free every three months. Third-party platforms such as ClearScore also let you track your score at no cost.

Once you know your position, there are quick steps you can take to improve your profile before applying:

- Check for errors: Review your credit report carefully and correct any inaccuracies with the bureau. Even a small error, like outdated ABN details, can affect your score.

- Show positive cash flow habits: Pay suppliers, invoices, and tax obligations on time for at least 3–6 months to demonstrate repayment discipline.

- Prepare your paperwork: Having BAS, financial statements, and a clear business plan ready shows stability and helps speed up the application process.

For more guidance, see Prospa’s blog on how to improve your credit score.

Ready to turn your credit score into an opportunity?

A strong business profile is the most important factor when it comes to funding; your credit score is only part of the story. By showing healthy cash flow, reliable revenue, and a clear plan for growth, you’ll be in a strong position to secure finance that supports your goals.

Now that you know what lenders look for, you can check if you’re eligible for a Prospa loan in minutes with no impact on your credit score.