At a glance

- Strong originations of $128.5 million, up a significant 61.8% on the prior corresponding period (“pcp”) (1Q21: $79.4 million).

- Despite ongoing COVID-19-related lockdowns in key regions throughout Australia and New Zealand, Prospa achieved $41.8 million of originations in July, $44.9 million in August and $41.8 million in September.

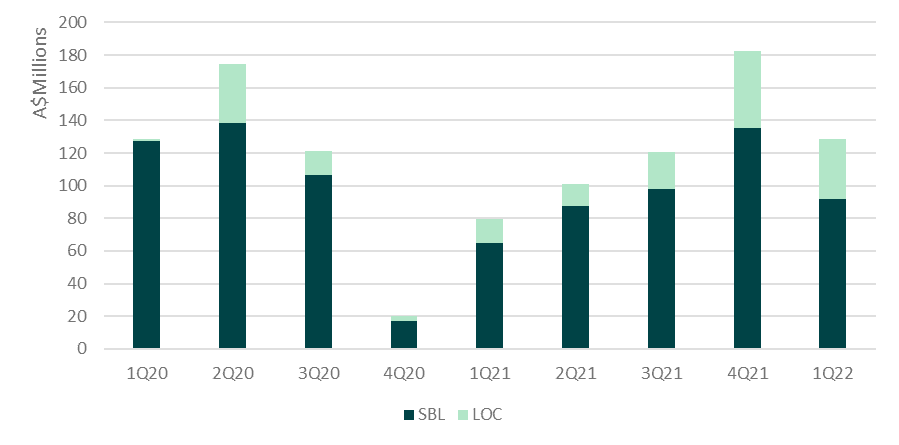

- Of the total originations for the quarter, 71.5% were derived from Prospa’s Small Business Loan, and 28.5% from the Company’s Line of Credit product.

- The New Zealand business performed strongly with originations of $22.1 million in the quarter, a significant 275% increase on 1Q21 ($5.9 million).

- Average Gross Loans increased to $436.7 million during the quarter, up 11.0% on the prior quarter (4Q21: $393.5 million), with an annualised portfolio yield of 34.3%. Closing Gross Loans accordingly increased to $442.2 million, up 3.5% on the prior quarter (4Q21: $427.1 million).

- Total revenue before transaction costs increased to $37.8 million, up 13.2% on the prior quarter (4Q21: $33.4 million).

- Continued to demonstrate a loyal customer base with repeat and returning customers accounting for 49% ($63.3 million) of total originations. Importantly, these customers represent a lower cost of acquisition than new customers to Prospa. Total active customers increased to a 2021 high of 12,200.

- Long term relationship development continued to be essential for growth with the Company’s customer-centric approach resulting in a Net Promoter Score above 80[2]. Note positive customer sentiment remains an important driver of originations.

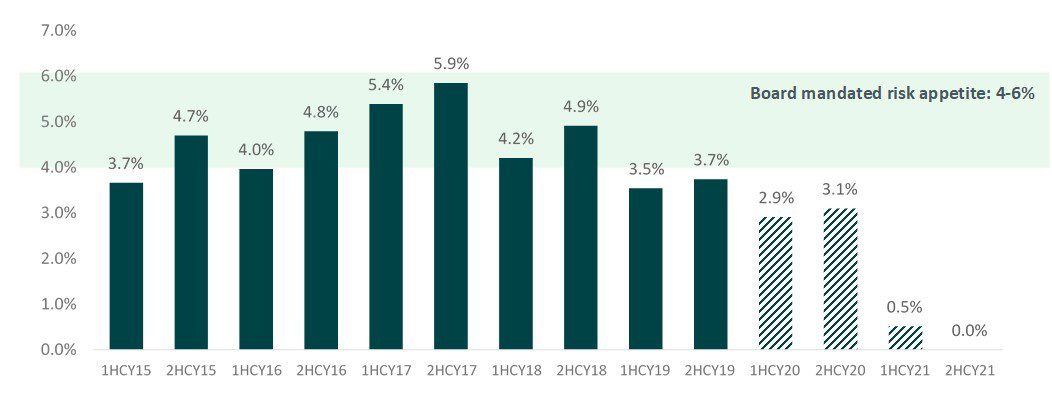

- Reflecting continued economic recovery and resilient portfolio performance, credit provisioning for future bad debts remained at 7.9% of total loans.

- Overall growth was underpinned by Prospa’s strong balance sheet and funding platform, with $581.8 million[3] in available third-party facilities ($194.4 million in available undrawn facilities) and $93.0 million of cash (of which $53.3 million is unrestricted).

- During the quarter, Prospa also issued and priced its first public term Asset Backed Securitisation of $200 million to wholesale investors, supported by a pool of Australian Small Business Loans and Line of Credit facilities.

Prospa Group Limited (ASX: PGL) (“Prospa” or “Company” or “Group”) is pleased to provide a trading update for the quarter ended 30 September 2021 (“1Q22”), with this quarter’s results driven by strong sales efforts capitalising on continued economic recovery, prudent expense management and ongoing investment into technology [1].

Greg Moshal, Chief Executive Officer, said:

“I am proud to report that Prospa has achieved strong results this quarter with SMEs displaying their resilience and ability to navigate through the ongoing effects of COVID-19. Despite two of Australia’s major cities remaining in lockdown during the quarter, pleasingly, we have seen positive sentiment sweeping the SME market as we enter a phase of strong economic recovery that is translating to very strong origination and revenue performance. With this momentum in quarterly revenue growth, underpinned by our investment into technology and our continually evolving award-winning suite of products, we are excited to continue to deliver on our promise to help small businesses grow, run and pay.

Prospa’s 1Q FY22 results were a direct result of our products providing an enhanced and market leading experience for our customers throughout Australia and New Zealand, with our smarter and faster credit decision engine now leveraging the broad range of learnings and insights obtained throughout FY21. Importantly, active customers reached a record high for 2021 of 12,200, noting c.50% of originations were derived from repeat business. Customer satisfaction was further evident in our NPS score of over 80.

Looking ahead, the business is well placed to continue to execute on growth. I am encouraged by the initial response received following our recent Investor Day and planned release of our new lending solutions and innovative cash flow management and payment products.”

1Q22 financial performance

Loan originations of $128.5 million were up 61.8% on pcp (1Q21: $79.4 million), noting demand for Prospa’s Line of Credit comprised a record 28.5% ($36.6 million) of the total, with the Small Business Loan driving the remaining 71.5% ($91.9 million). Importantly, 49.3% of originations ($63.3 million) were derived from repeat or returning customers during the quarter, reflecting a materially lower cost of acquisition than new customers.

Quarterly originations by product[4]:

The New Zealand business continued to perform strongly, contributing originations of $22.1 million to the total, representing a significant increase of 275% on pcp (1Q21: $5.9 million). Strong performance in the region further validates Prospa’s decision to expand its product offering in this market.

Average Gross Loans of $436.7 million increased by 11.0% on the prior quarter (4Q21: $393.5 million), underpinned by strong originations. Closing gross loans for the quarter reached $442.2 million, up 3.5% on prior quarter and only 7% lower than the highest gross loans balance on record for Prospa (refer February 2020: $475.4 million). The quarter’s annualised portfolio yield remained strong at 34.3%, driving strong corresponding revenue performance for the period.

Total revenue before transaction costs trended in line with growth in average gross loans, reaching $37.8 million for the quarter, up 12.9% on the prior period (4Q21: $33.4 million) and increased 34.5% on pcp (1Q21: $28.1 million). The business expects revenue to continue to trend in line with portfolio growth and the introduction of various new products and capabilities.

Following a period of prudent expense management, operating expenses declined 9.1% on the prior quarter to $19.0 million. Moving forward, Prospa will continue to invest in enhancing its technology, diversifying its product suite, and driving sales and marketing initiatives across the Group.

Quarterly key metrics

Trust facilities (as at 30 September 2021):

| Facility ($m) | Facility Limit | Drawn | Maturity |

| Propela Trust (AU Warehouse) | 27.0 | 7.3 | Mar-22 |

| PROSPArity Trust (Warehouse Facility) |

135.0 | 21.9 | May-24 |

| Pioneer Trust (Warehouse Facility) |

138.8 | 106.4 | Feb-23 |

| PROSPArous 2021-1 (Rated ABS Term) | 190.0 | 190.0 | Feb-24 1 |

| Kea Trust 2021-1 (NZ) | 30.2 | 30.2 | Sep-24 |

| Kea Trust 2021-2 (NZ) | 60.1 | 30.9 | Aug-24 |

- Call option date. Final maturity is December 2026.

Stable static loss rates by cohort at 30 September 2021:

Represents static loss rates net of recoveries at 30 September 2021 for the Australian Small Business Loan and Government Guarantee Scheme loan products (previously excluded). Banded columns reflect cohorts that are still seasoning.

[1] Note all figures in AUD unless otherwise specified.

[2] Average for the period 1 July 2021 to 30 September 2021.

[3] NZD converted at RBA exchange rate 0.954 as at 30 September 2021.

[4] Fresh originations from all products and geographies as at 30 September 2021. Small Business Loans (“SBL”) includes Back to Business Loans originated under the Australian Government Guarantee Scheme and the New Zealand Business Finance Guarantee Scheme. Line of Credit (“LOC”) includes Back to Business Lines originated under the Australian Government Guarantee Scheme.